It was once the norm for an aspiring start-up to seek funding through venture capital (VC). Ownership of the company would be divided amongst participating investors via limited partnerships established by the VC firm, while those investors would often remain invested in the company for years.

But in the last 18 months or so, it’s fair to say that for those start-ups utilizing blockchain technology, the global craze for Initial Coin Offerings (ICO) has drastically alteredthe fundraising landscape. Although first emerging in 2013, ICOs didn’t truly burst onto the scene until last year, as new cryptocurrency-based projects began raising tens, if not hundreds,of millions of dollars from investors. These projects are typically put together with little more than a whitepaper, a website, a roadmap and a development team.

According to CoinSchedule stats, ICOs raised nearly $4 billion last year– substantially more than the $95 million raised in 2016. And already 2018 has managed to dwarf last year’s figure, with the Telegram token sale leading the charge towards a $12.5 billion total to date. What’s more, the 210 ICOs that were held in 2017 already pales in comparison with the 594 held so far this year.

What’s even more remarkable is that last ICOs shot passed VCs last years in terms of funds raised by blockchain projects. In the 14 months to February 2018, Crunchbase observed that blockchain and related start-ups raised nearly $1.3 billion in traditional VC rounds worldwide; whereas for ICOs, a whopping $4.5 billion was raised:

As such, ICOs today not only present a significant challenge to VCs as far as blockchain start-up financing is concerned, they are attracting considerably more investor interest. And while this dramatic shift is raising important questions for both start-ups and investors about their funding preferences, it is also raising concern over the future of VCs. But is this concern justified?

The case for ICOs

- Arguably the most exciting advantage ICOs possess vis-à-vis VCs is that virtually everyone (that is, those with an online connection and enough money to buy a token) can invest in the majority of ICOs. Token offering events have proven to represent a genuine opportunity for anyone to make a heap of money over a short time horizon, irrespectiveof their financial position or level of investor accreditation. VCs, on the other hand, tend to serve the wealthier investor segments – institutions such as hedge funds and private equity firms, as well as high net worth individuals – while they will usually require a substantial initial outlay to even be considered.

- Another clear benefit of ICOs is the liquidity that start-ups can obtain in record time. Presuming ICO investors receive their tokens as planned, secondary market trading will commence as soon as the project lists its token on cryptocurrency exchanges. And in turn, the project has a chance to obtain instant liquidity. VC-funded projects, however, remain relatively illiquid until funds become available again, either upon an exit through a sale or an IPO. Investors, therefore, have to wait before being able to monetize their investment.

- Furthermore, ICOs offer a directness between companies and their stakeholders that was not previously possible. While investors have the opportunity to “get in on the ground floor” of a project’s success, they also provide the start-up with a community of potential users for its blockchain product when it goes live. The VC model doesn’t offer the same kind of efficiency.

- And of course, let’s not forget the returns that ICOs are generating. For most investors, they have been astronomical. VC/PE firm Mangrove Partners had found that until October 2017, “if one blindly invested €10000 in every visible ICO, including the significant number of ICOs that failed, this would have delivered a +13.2 times return”. A more recent Boston College study of ICOs, meanwhile, found evidence of “significant ICO underpricing, with average returns of 179% from the ICO price to the first day’s opening market price, over a holding period that averages just 16 days.” Again, such gains are unequivocally phenomenal.

With such perks offered up by ICOs to both start-ups and investors, it’s not surprising that questions are being asked about the future viability of the VC model. Indeed, if investors are making many multiples in returns on their ICO investments, and start-ups are flush with millions of dollars, then surely both parties are happy? And thus, surely the utility of VCs will become severely diminished going forward? Not quite…

The case for VCs

- While ICOs may be exploding, VC financing for blockchain start-ups has also boomed. According to Pitchbook, 2017 brought with it “a record amount of venture capital—more than $1 billion”—to start-ups in the cryptocurrency sector, while in the 2 years through 2017, “179 US investors had participated in at least one VC deal for a crypto start-up.” And much like the trend displayed by ICOs, this year has also seen the amount of money raised through VC rounds by blockchain and blockchain-adjacent start-ups easily surpass the 2017 total:

- Of course, no discussion about ICOs can be complete without highlighting the distinct lack of regulatory clarity surrounding the space at present. While the SEC and other watchdogs around the world are now moving to remedy this situation, especially with regards to classifying the tokens being issued as securities or utilities (as I’ve previously discussed), official rules for the space are not yet set in stone. Conducting sufficient due diligence, therefore, becomes a problem, and explains why institutional investors have remained distinctly averse to ICOs thus far. While it’s refreshing to see everyone being able to participate in an ICO, therefore, it also means that funding is unlikely to contain much ‘smart money’.

- The ICO space continues to be plagued by scams. A recent study from ICO advisory firm Statis Group revealed that over 80% of ICOs conducted in 2017 were identified as scam projects. And that Boston College study also found that about 56% of ICO-funded start-ups die within four months of hosting their token sale events. Clearly, that’s not great news for long-term investors. Such figures also severely tarnish the reputation of ICOs and can sap investor confidence in certain projects, especially if KYC and AML requirements are also absent from the fundraising process. In contrast, the addition of a VC in a new project represents a strong indication of the legitimacy of a project. A VC firm with a strong track record can provide that confidence to a potential investor, and indicates that there will be structured financial support through the next stage(s) of a project’s development timeline.

- The value of VCs is not only reflected by their monetary support. They also provide technical and managerial expertise to companies during their most precarious stage of development. The nature of funding – i.e. through a series of specific rounds – is also likely to ensure the development of the company is more structured than were it to receive a huge lump sum at up-front, à la an ICO.

- It is worth clarifying that ICOs represent a fundraising mechanism for blockchain start-ups. And more specifically, token-issuingblockchain start-ups. If you are deliberating over which fundraising mechanism is the most appropriate, it is certainly worth asking yourself whether your blockchain company actually needsto use a cryptocurrency model. If it’s not appropriate, then VCs, or other forms of financing are likely to be more suitable. The cryptocurrency complex is already overflowing with tokens that seemingly have no inherent value; simply issuing a token for no reason does little to advance the reputation of cryptocurrency as an asset class.

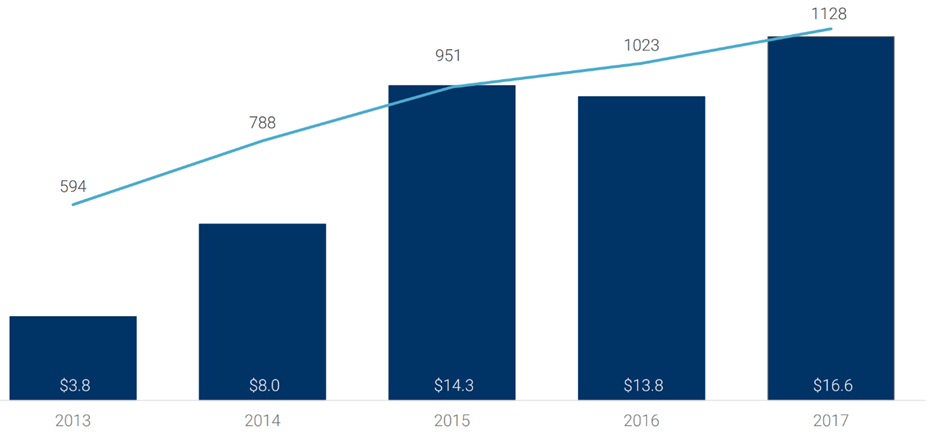

- When looking at the fintech realm as a whole, not all (indeed, not even most) new companies are adopting blockchain. And so even in the unlikely event that ICOs do end up overwhelmingly dominating the blockchain space, VC will continue to play a dominant role in the funding of new ‘non-blockchain’ tech companies. Indeed, as CB Insights recently showed, VC in the wider fintech sector continues to thrive:

Annual global VC-backed FinTech deals and financing, 2013 – 2017 ($Billion)

While ICOs represent a disruptive and exciting development in the evolution of start-up funding, VCs continue to offer their own distinct set of benefits that simply can’t be replaced by the new kid on the block.

At the same time, the emergence of ICOs should also present an opportunity for the VC model to evolve. For example, we may well see greater collaboration between VCs and ICOs as part of a mutually beneficial relationship. During a company’s early stages, receiving expertise from experienced VCs has traditionally been an important part of the funding process; it shouldn’t be any different for a blockchain start-up. And as for the VC firm itself, partnering with an ICO project could allow it to participate in a potentially lucrative project early on, and perhaps even allow it to receive favourable terms should it invest in the token sale. Indeed, such a trend already seems to be emerging, as more blockchain platforms appear keen to raise equity to fund marketing and development prior to hosting their ICO.

Ultimately, as far as the blockchain space is concerned, the meteoric rise of ICOs should not merely be seen as a threat to VCs. Rather, it should open up opportunities for collaboration and evolution of the start-up finance sector. And it will be fascinating to see how it plays out.

Some really wonderful info , Gladiolus I observed this.

What’s up to every body, it’s my first pay a visit of this weblog; this website contains remarkable and genuinely fine material for visitors.

Magnificent site. Lots of helpful information here. I

am sending it to some pals ans also sharing in delicious.

And obviously, thanks on your effort!