Diversification in Investing, Gender Politics, Your Workplace, and Your Private Life: The Unexpected Consequences of Not Putting All Your Eggs in One Basket

Olegs Jemeljanovs, PhD, CFA·11 min

Post 2008, as Regulators grappled with the idea of coming up with a new effective regulatory model, an explosion of Fintech development took place, and this exponential growth in Fintech caused a major challenge for the regulators. Since the whole idea of Fintech was the disruption of the pre-existing models of Markets, Industries & Finance in general it was in direct contrast with the regulators sole aim of preventing any sort of disruption in the markets. But at the same time there has been a strong regulatory focus on encouraging innovation & development in the financial system too. Therefore the regulators had to find a middle ground to encourage innovation while dealing with the challenges that emanate from the adoption the new technologies. They have been trying to balance the innovation & growth with the financial stability & consumer protection.

To enforce this new vision the regulators adopted four major approaches:

Post 2008, as Regulators grappled with the idea of coming up with a new effective regulatory model, an explosion of Fintech development took place, and this exponential growth in Fintech caused a major challenge for the regulators. Since the whole idea of Fintech was the disruption of the pre-existing models of Markets, Industries & Finance in general it was in direct contrast with the regulators sole aim of preventing any sort of disruption in the markets. But at the same time there has been a strong regulatory focus on encouraging innovation & development in the financial system too. Therefore the regulators had to find a middle ground to encourage innovation while dealing with the challenges that emanate from the adoption the new technologies. They have been trying to balance the innovation & growth with the financial stability & consumer protection.

To enforce this new vision the regulators adopted four major approaches:

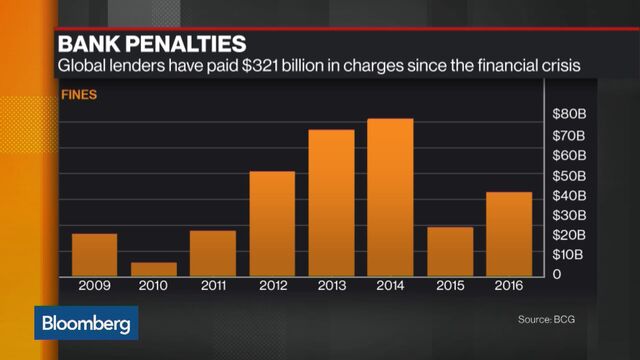

Ever since the financial crisis of 2008 we have seen an enormous amount of new regulations around the world with new regulations coming out of a major jurisdiction every hour resulting in thousands of new regulations every year, which becomes a big hassle for a financial institution doing business on a cross-border basis. This causes a major hindrance in their operations and a drop in their profitability apart from the costs associated with the compliance. This has driven the established financial industry to apply technology to address their compliance requirements & the associated costs by seeking the assistance of new startups who can address their problems of regulatory & compliance burdens. Regulators themselves are increasingly using technology to do a better job in their regulatory functions.

The bigger issue with regards to RegTech still remains to be the one where there is a joint or uniform regulatory framework across different jurisdictions so it becomes easier for the companies to function effectively while the regulators can enforce the regulations in a streamlined fashion. Recent developments are pointing towards creation of such an initiative which will not only encourage innovation but also allow companies to launch their products in multiple jurisdictions at the same time without the need of having to comply to a different set of regulations. Global ‘fintech sandbox’ has brought together 12 regulatory authorities across the globe to share policy ideas & keep up with the advancement of new technologies to be in a better position to tackle the issue of uniform regulatory framework.

Ever since the financial crisis of 2008 we have seen an enormous amount of new regulations around the world with new regulations coming out of a major jurisdiction every hour resulting in thousands of new regulations every year, which becomes a big hassle for a financial institution doing business on a cross-border basis. This causes a major hindrance in their operations and a drop in their profitability apart from the costs associated with the compliance. This has driven the established financial industry to apply technology to address their compliance requirements & the associated costs by seeking the assistance of new startups who can address their problems of regulatory & compliance burdens. Regulators themselves are increasingly using technology to do a better job in their regulatory functions.

The bigger issue with regards to RegTech still remains to be the one where there is a joint or uniform regulatory framework across different jurisdictions so it becomes easier for the companies to function effectively while the regulators can enforce the regulations in a streamlined fashion. Recent developments are pointing towards creation of such an initiative which will not only encourage innovation but also allow companies to launch their products in multiple jurisdictions at the same time without the need of having to comply to a different set of regulations. Global ‘fintech sandbox’ has brought together 12 regulatory authorities across the globe to share policy ideas & keep up with the advancement of new technologies to be in a better position to tackle the issue of uniform regulatory framework.

Related Articles: TechFin vs. FinTech – What’s the difference?, The rise of P2P Finance model, Evolution of Fintech — A timeline, The ABCDs of Fintech

Stay in touch: Twitter | StockTwits | LinkedIn | Telegram| Tradealike

Faisal is based in Canada with a background in Finance/Economics & Computers. He has been actively trading FOREX for the past 11 years. Faisal is also an active Stocks trader with a passion for everything Crypto. His enthusiasm & interest in learning new technologies has turned him into an avid Crypto/Blockchain & Fintech enthusiast. Currently working for a Mobile platform called Tradelike as the Senior Technical Analyst. His interest for writing has stayed with him all his life ever since started the first Internet magazine of Pakistan in 1998. He blogs regularly on Financial markets, trading strategies & Cryptocurrencies. Loves to travel.