We are living in a world increasingly driven by data in every aspect of our lives with emerging technologies like Artificial Intelligence, Big data, Blockchain & Cloud computing acting as the driving forces behind this digital transformation. These technologies are not only helping us streamlining the automation of the current processes in different industries & sectors of the economy, but also help us in managing the copious amounts of data being produced by them. The amalgamation of these technologies & the relentless automation has given rise to “Digital Identity” which would be one of the most impactful technology in the coming years. A very simple example in this regard has been how our personal identification documents like the passports have evolved over the past couple of decades from being a simple booklet to a Machine-readable document to one which has chip incorporated in it with all your data stored on it.

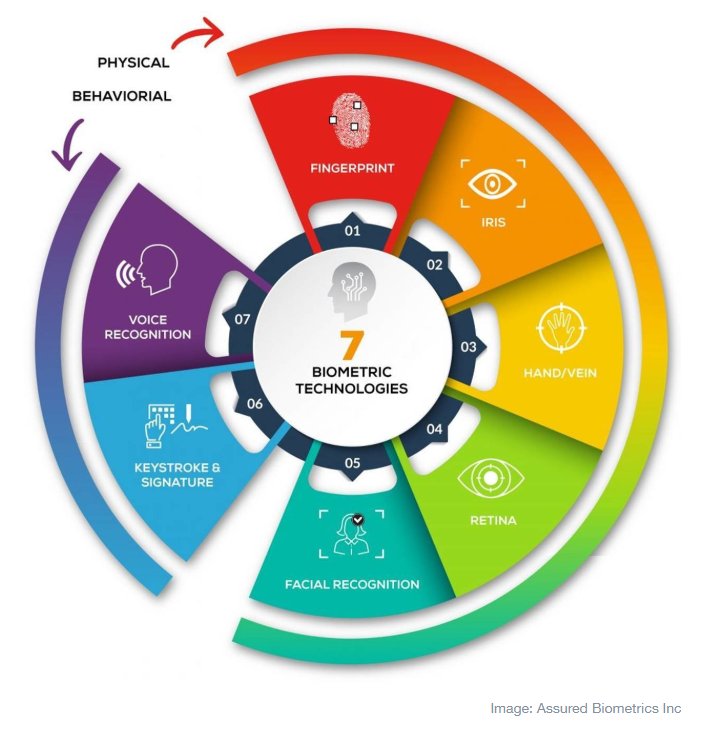

Identity these days takes a much more complex shape with the inclusion of Physical, Legal, Electronic & Behavioral aspects combined; some of which are derived from data-driven metrics. Let’s take a brief look at these four components of the Identity. They are sub-categorized further into static & dynamic identities. Static identity defines unique & non-changeable features while dynamic component pertains to the evolving nature of one’s habits.

-

Physical identity – Fingerprints, IRIS scanner, DNA (static)

-

Legal identity – Your Passport, Photo ID (Driving License etc. – static)

-

Electronic identity – Social media Profiles (Facebook, Twitter etc. – dynamic)

-

Behavioral identity – the way you communicate, online shopping etc. – (dynamic)

The static identity metrics have been used for a long time especially in the context of financial institutions. Let’s say for example when you go to open an account with a bank, they will get to know you, when you provide them your legal identity & fill out the KYC (Know your Client) documentation. Electronically, however, they will only get to know you when you do online banking with them or buy other financial products etc. So unless you transact with bank often or already have a bank account with them, there is no way of them having an access to your behavioral or electronic identity.

Some of the Fintech startups have filled this void and are using advanced data analytic techniques utilizing the behavioral & electronic identities to provide credit analysis to financial institutions & banks, which provider deeper insights into consumers’ behavior so that customized, relevant & tailored solutions which meet their needs & requirements could be provided to them. An example in this regard is WeBank — China’s First Online only bank which uses sophisticated credit analysis based on the WeChat’s social media usage & online purchase patterns of their customers.

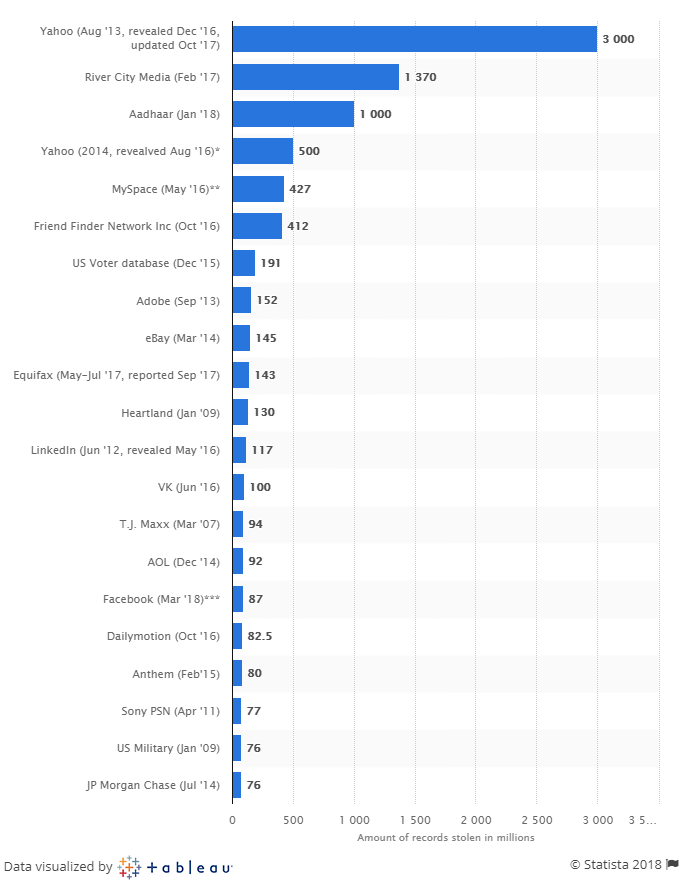

Privacy & Protection of the customers’ data has become one of the biggest challenges for companies like Financial institutions & tech companies who have large user bases and tons of personal & sensitive data regarding their clients stored on their servers. In the past few years alone the frequency of the security breaches & hacks has highlighted this issue & the associated challenge of protecting the digital data of their clients. Equifax’s (credit monitoring company in U.S.) massive security breach, which led to the exposure of the data of 143 million Americans is the most high-profile case of such a breach in recent history, where personal financial information of almost 1 in 2 Americans became public knowledge.

Coming back to the benefits of the digital identity – the mere inclusiveness that this form of identification has brought to billions of people in the developing countries is nothing short of revolutionary. More than 1.2 billion in developing countries have no form of formal identity, therefore, they couldn’t enter the financial services industry or any other sector where such documentation was required. A simpler, more efficient process was required to identify a person & authenticate a transaction. One such ambitious project was undertaken in India where 99% of the population over 18 is now provided with a 12 digit number representing their bio-metric & geographical data. Using this digital identity, Indian citizens can make online bill payments, authorize money transfers, register for an online course or fulfill KYC requirements electronically.

A similar initiative was launched in Nigeria where Civil Services department has started using digital identity for its employees to combat the increased instances of identity theft which was leading to either someone receiving two times the salary or receiving someone else’s salary. Since the implementation of the digital identity pilot, the government has saved over $75 million.

And finally in Europe where comprehensive consumer data regulations were introduced in the form of PSD2 (Second Payment Services Directive) & GDPR (General Data Protection regulation) which outline how the data of consumer will be used by the companies. The combination of both these regulatory frameworks puts the individual at the center of the financial services industry & and in control of their personal data. So if an individual wants to give access to their bank account to a merchant they can do so, by-passing the traditional banking network. Once the reforms are completed, the final step would be the aggregation of Physical, Legal, Behavioral & electronic data into a single digital wallet which we individuals will control – by granting access to companies or deciding to monetize from it.

We are moving from a model where we trade data for convenience to one where we trade it for compensation. Therefore finance is being changed & digital identity alongside with it. And while a lot of people are still uncomfortable with the intrusive nature of digital identities which in the wrong hands can completely manipulate their lives, it provides huge advantages & efficiency, and European regulations like GDPR & PSD2 certainly help in allaying those fears and is a step in the right direction.

Stay in touch: Twitter | StockTwits | LinkedIn | Telegram| Tradealike