You are bound to hear two very different opinions about the current global financial system depending on who you ask, a person with a good job, nice house & a stable income living somewhere in the Western hemisphere or a small farmer living in the remote regions of Africa or South Asia. While the former would probably boast of stability, financial prosperity & opportunity to make money, the latter might complain about barriers to entry, inequality & high costs to being hindrances for inclusion into the system. While the current financial system has weathered a few storms & it has been a better choice than some its predecessors or proposed systems comparatively speaking, the time has come when it is beginning to show signs of crumbling. The technological revolution & the ongoing automation is perhaps the tipping point which is going to help revamp this rotten old model and help develop a new financial ecosystem that brings inclusiveness, equality & progress for all. Let's review some of the weaknesses of the current global financial system & how are they being addressed.

The Unbanked

The traditional brick & mortar banks have been the central point of access to all sorts of financial services since their advent - bill payments, wealth management, investing, retirement planning etc. With a burgeoning middle class in the developing World & a rapidly growing population in Africa, banks have been unable to keep up with this growth & provide access to these basic financial services to all. According to a 2017 survey, 1.7 billion people around the World still remain unbanked & therefore cut off from the mainstream financial system - a majority of these people cited lack of money & trust, high fees & accessibility as the biggest reasons for not having a bank account. Financial exclusion is perhaps the biggest & most pressing issue facing the financial system. This trend, however, is shifting slowly with the advent of alternative solutions like digital-only banks. Fintech enabled digital financial services are making great progress in bringing this unbanked segment of the society towards financial inclusion.

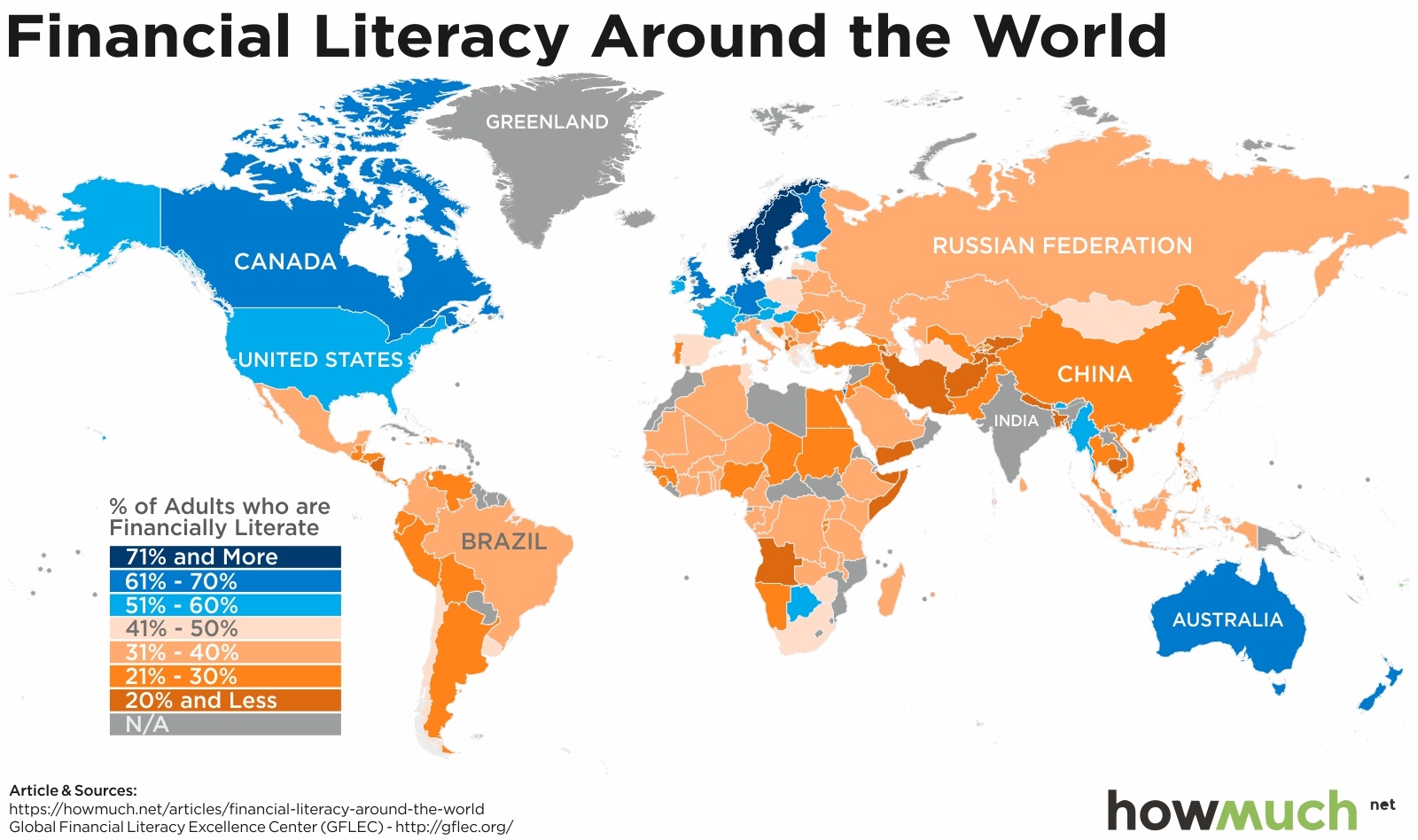

Global Financial literacy

Being Literate is one thing but being financially literate is entirely another ball game. According to a recent global survey, on average, ONLY one in three people understand the basic financial concepts & most of the financial literacy is concentrated in the advanced economies (figure below) which is evident from the skewed distribution of wealth around the globe. It is ironical indeed that in such an advanced age of STEM (Science, Technology, Engineering & Mathematics) education, the majority of the population still lacks the basic skills of personal financial management, investment & the working of the financial markets in general. Even in western schools nothing is taught about good financial habits, managing your credit score or saving. Without the right tools & knowledge how can you expect the population to make the right decisions regarding money matters or building wealth for that matter. A lot still needs to be done on this front to increase awareness among the masses about the creation of wealth & their general financial well-being.

High Costs & Slow transactions

Of course having access to financial services is part of the story. The costs associated with the conducting business with the banks & related financial institutions is the other part of the equation. One would expect storing money & transferring it would be cheap, fast & convenient but the experience says something else about the current banks. High costs of maintaining bank accounts with even higher remittance fees structure are anything but convenient. According to the World Bank report the global average remittance fees is around 7% significantly higher than the G-20 objective of 5% & and the UN Sustainable goal target of 3%. Even more inconvenient is the time it takes for the processing of cross border transfers. Notable to see, however, that the remittance fees have been steadily falling in recent years from the increased competition & digitization of financial services. No wonder that the low-cost & efficient Fintech providers are taking up the space of traditional banks by winning the trust of the users.

Lack of Trust

According to a recent survey of the different sectors of the global economy Financial services is the least trusted one by the people. This combined with even lesser trust by the people in their governments (especially in the western countries) withers away their confidence in the Central banks, mainstream banks & other financial institutions. There is an actual backdrop to this situation - the most famous & notorious financial meltdown of the recent times & perhaps second only to the Great Depression started in Sep. 2008 in the U.S. The biggest catalyst was the sub-prime mortgages that were doled out to people with questionable credit, leading to an unsustainable housing market bubble which ultimately popped. The complacency that emanated from years of stable growth, low inflation & high employment rates in the U.S brought the financiers to lend recklessly. The Federal Reserve (U.S central bank) was in the picture before, during & after the mess.

The easing cycle that started in May 2000 to Dec. 2001 saw interest rates dropped to 1.75% from 6.0% creating an influx of “easy money” in the economy — which the greedy bankers were ready to distribute! The irony is the general public still thinks the financial institutions haven't learnt any lesson from this mess as they continue to conduct shady deals, dodge compliance procedures & overlooking internal and external controls. On the other side of the spectrum, the technology companies have the biggest trust of the consumers & that is the primary reason their shift to providing financial services is proving successful.

Rising Global Inequality

The biggest critique for the current Global financial system emanates from the fact that Rich is getting richer & the Poor are getting poorer. In simpler terms, the global wealth is concentrated in the hands of a very few people who have access to financial expertise, informational advantage, capital to invest & access to varied asset classes & varied financial opportunities. While the majority struggles to make ends meet & lives paycheck to paycheck, with little money to spare and lack of access & opportunities, the creation of wealth is a far-fetched dream for them. Actually, the statistics in this regard are staggering with the top 1% of the wealthy controlling 47% of the global wealth.

Financial Censorship & Manipulation

In a centralized financial system, like the one we have currently the governments have the power to manipulate it which can have devastating effects on the financial markets & the lives of the people. The most recent example is of Venezuela where hyperinflation has wreaked havoc with the economy of the country & the lives of its people. Fighting International economic sanctions, the government began to devalue the currency periodically which eventually led to uncontrollable hyperinflation crossing a staggering 2.5 million percent. This runaway hyperinflation resulted in a complete loss of trust in the country's fiat currency, caused a recession, evaporated people's savings & increased crime rate resulting from a sky-high unemployment rate of 39% (IMF). The governments can also use this central system to financially censor their citizens by freezing accounts, removing funds, denying access to payment systems etc. In a yet another desperate & centralized move the Venezuelan government issued an Oil-backed digital currency (Petro) to be the equivalent of the national fiat currency. Even strict enforcement by the government to use Petro has not born fruit as people continue to trust & increasingly use the decentralized mainstream cryptos.

Increased Systematic Risk

One final but a very important drawback of the current financial system is that financial power is in the hands of few institutions like the Central banks or big bank names which are too big to fail. We will have to go back to the example of 2008 financial meltdown when the U.S government bailed out multiple big companies for billions of dollars as their fall would have had a ripple effect on the entire global financial system causing a catastrophe. All these risks & drawbacks have been well-known but without a real alternative there was no choice but to continue with the current system. That is about to change.

While there is no doubt that the centralized nature of the current global financial system has helped in creating enormous amounts of wealth for people who had access, knowledge & connectivity to the system, it also created global challenges like inequality & lack of access to basic financial services for others. The good news is that with the proliferation of smartphones & internet access combined with the development of decentralized technologies like Blockchain is enabling us to completely overhaul the current global financial system & replace it with a new financial ecosystem which is fair, equitable & accessible to all.

Email?|

Twitter?

| LinkedIn?

| StockTwits?

| Telegram?