Diversification in Investing, Gender Politics, Your Workplace, and Your Private Life: The Unexpected Consequences of Not Putting All Your Eggs in One Basket

Olegs Jemeljanovs, PhD, CFA·11 min

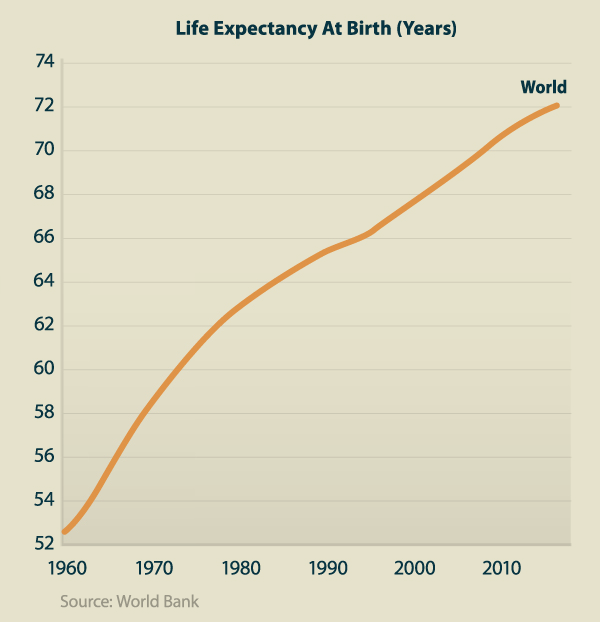

Despite the data, people still underestimate their life expectancy for two reasons - comparing themselves to older relatives & quoting life expectancy at the birth statistic, both of which are misleading... here's Why? According to U.S Library of National Medicine, only 25% of the variation in lifespan is based on ancestry, but it's certainly not the only factor. Gender, lifestyle, Diet are some of the other factors that contribute towards your lifespan. For the second metric, people fail to realize is that while their expected lifespan might be shorter at the time of their birth but it continues to increase during their lifetime. According to an OECD study for expected Age of death as of 2016 in the U.S climbed from 72 to 86 for Men & 82 to 89 for Women during their lifetime. Couple the longer lifespans & inaccurate life expectancy predictions with the lack of retirement savings in the U.S households (figure below) & we have a bigger problem at our hands. According to the data, 35% of the U.S households don't even have any retirement savings whatsoever. This is where Longevity Risk enters into the picture.

Despite the data, people still underestimate their life expectancy for two reasons - comparing themselves to older relatives & quoting life expectancy at the birth statistic, both of which are misleading... here's Why? According to U.S Library of National Medicine, only 25% of the variation in lifespan is based on ancestry, but it's certainly not the only factor. Gender, lifestyle, Diet are some of the other factors that contribute towards your lifespan. For the second metric, people fail to realize is that while their expected lifespan might be shorter at the time of their birth but it continues to increase during their lifetime. According to an OECD study for expected Age of death as of 2016 in the U.S climbed from 72 to 86 for Men & 82 to 89 for Women during their lifetime. Couple the longer lifespans & inaccurate life expectancy predictions with the lack of retirement savings in the U.S households (figure below) & we have a bigger problem at our hands. According to the data, 35% of the U.S households don't even have any retirement savings whatsoever. This is where Longevity Risk enters into the picture.

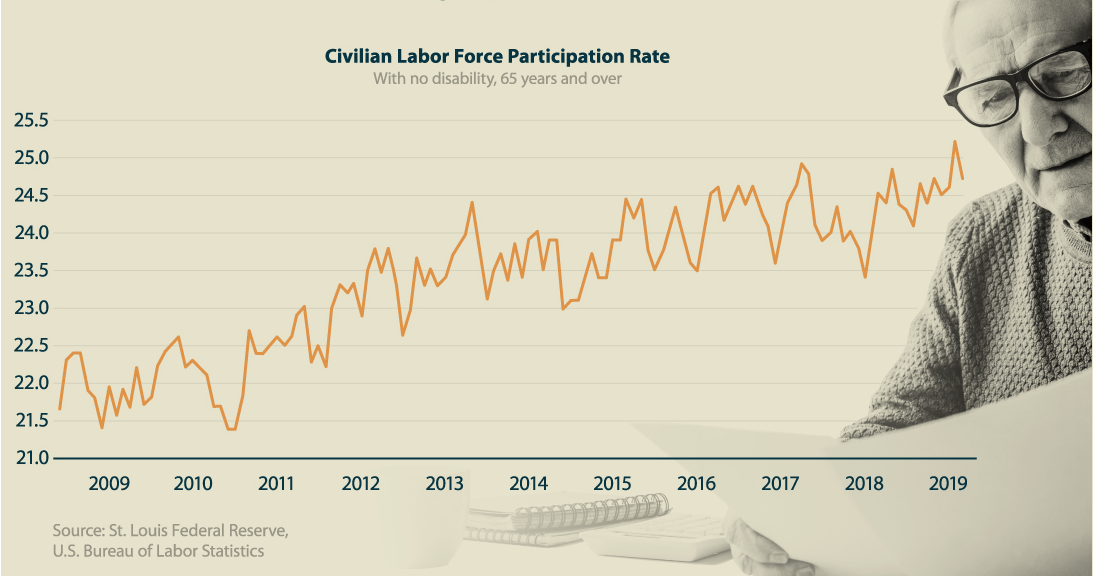

Combining all these factors many people are facing a real problem of outliving their savings. To combat this situation, the simplest & most common solution that is emerging is of Older individuals (over 65) are working longer to make up for the difference. This is evident from The Labor force participation rate for Seniors that has been steadily trending upwards for in the past decade in the U.S (figure below). But this alone can't combat the Longevity Risk. And to top all of this, the problem is not restricted to Seniors alone - according to Federal Reserve, 41% of the U.S Millennials (aged 18-29) have no retirement savings & prefer to keep cash.

Combining all these factors many people are facing a real problem of outliving their savings. To combat this situation, the simplest & most common solution that is emerging is of Older individuals (over 65) are working longer to make up for the difference. This is evident from The Labor force participation rate for Seniors that has been steadily trending upwards for in the past decade in the U.S (figure below). But this alone can't combat the Longevity Risk. And to top all of this, the problem is not restricted to Seniors alone - according to Federal Reserve, 41% of the U.S Millennials (aged 18-29) have no retirement savings & prefer to keep cash.

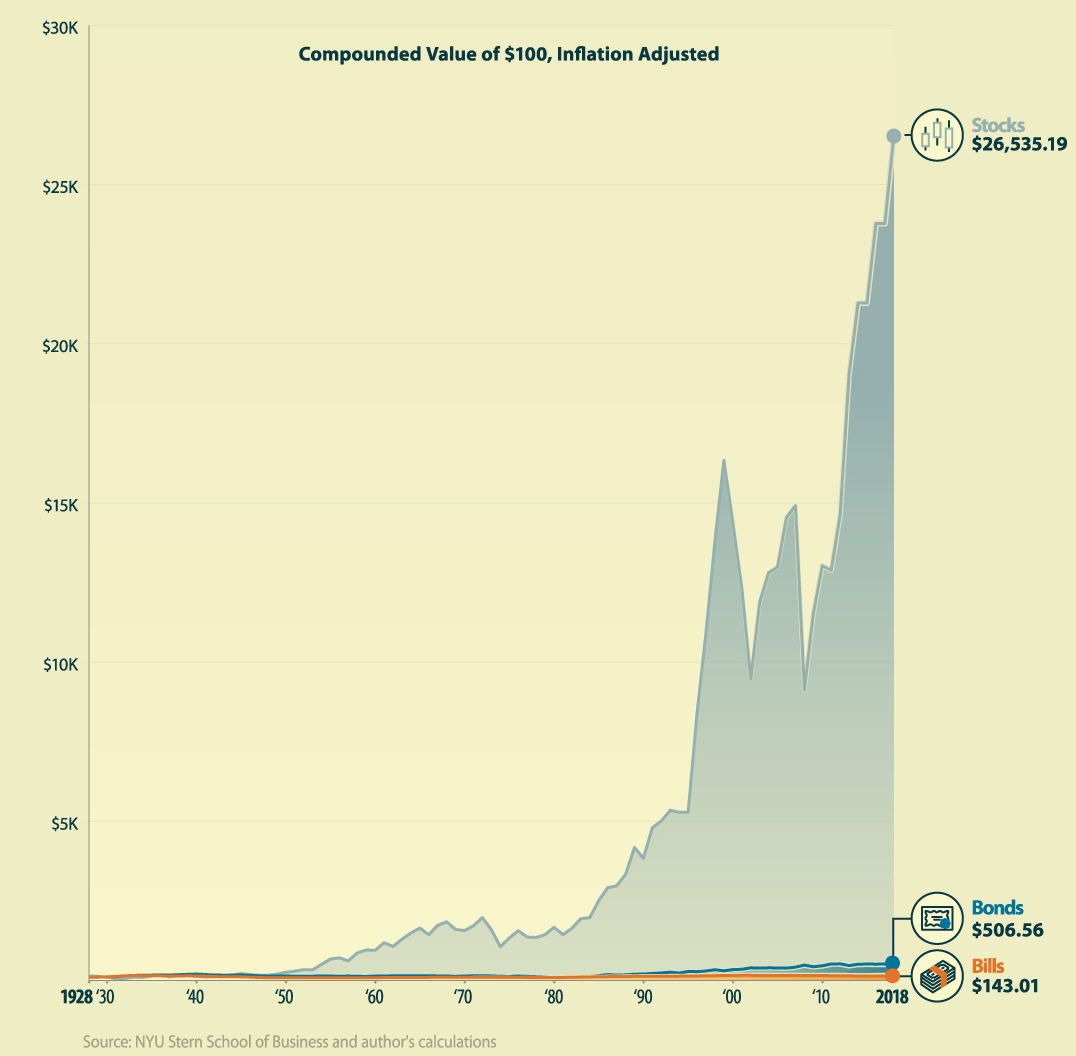

How do you solve this problem? One solution lies in the right mix of asset allocation in the investors' portfolio. The "100-age" rule provides a guideline on the kind of asset allocation mix one should have as the age progresses. Basically your age should match the proportion of stocks (high risk-high return) and bonds (low risk-low return) that one should have in their investment portfolio to manage risk exposure effectively. So for example, a person aged 25 who has just started working & looking at a long career in front of him would opt for 25% of bonds & 75% of stocks, since they are not risk averse at this stage of life & also looking for growth. On the other hand, a 65-year-old who is looking to retire soon would look at 65% of asset allocation to be in safe but low-risk investments since their aim at this age is the preservation of their retirement capital. With the rise in life expectancies & lengthening time horizons, Financial advisers are even suggesting a 110 or 120-age rule to their clients.

How do you solve this problem? One solution lies in the right mix of asset allocation in the investors' portfolio. The "100-age" rule provides a guideline on the kind of asset allocation mix one should have as the age progresses. Basically your age should match the proportion of stocks (high risk-high return) and bonds (low risk-low return) that one should have in their investment portfolio to manage risk exposure effectively. So for example, a person aged 25 who has just started working & looking at a long career in front of him would opt for 25% of bonds & 75% of stocks, since they are not risk averse at this stage of life & also looking for growth. On the other hand, a 65-year-old who is looking to retire soon would look at 65% of asset allocation to be in safe but low-risk investments since their aim at this age is the preservation of their retirement capital. With the rise in life expectancies & lengthening time horizons, Financial advisers are even suggesting a 110 or 120-age rule to their clients.

Simple rules of thumb as discussed above provide an easy understanding of the investment criterion, they shouldn't be treated as the only policy tool. Every person has a unique situation, risk profile, investment objectives, lifestyle & net worth which eventually dictate the overall make of their portfolio. Here are some of the things which can help reduce the Longevity risk.

Simple rules of thumb as discussed above provide an easy understanding of the investment criterion, they shouldn't be treated as the only policy tool. Every person has a unique situation, risk profile, investment objectives, lifestyle & net worth which eventually dictate the overall make of their portfolio. Here are some of the things which can help reduce the Longevity risk.

Faisal is based in Canada with a background in Finance/Economics & Computers. He has been actively trading FOREX for the past 11 years. Faisal is also an active Stocks trader with a passion for everything Crypto. His enthusiasm & interest in learning new technologies has turned him into an avid Crypto/Blockchain & Fintech enthusiast. Currently working for a Mobile platform called Tradelike as the Senior Technical Analyst. His interest for writing has stayed with him all his life ever since started the first Internet magazine of Pakistan in 1998. He blogs regularly on Financial markets, trading strategies & Cryptocurrencies. Loves to travel.