How did we get here? One big clue lies in the repo market.

We’ve found that people tend to forget (ourselves included) important factors, events, or definitions that are important for understanding what is happening in the current global theatre. In an effort to keep our readers’ comprehension fresh, we’ll cover some topics that may have been swept under the rug in light of the onslaught of new information that tends to bury us each week. The “throwback” topic for today is the repo market. Inspired by Anthony Pompliano’s podcast number 236, where he talks to Raul Pal and admits that repo markets are very confusing for him. Anthony is a prominent investor, so if this guy doesn’t know how repo markets work, then it’s someone’s job to fill the void!

After two months’ worth of major events such as COVID-19, negative oil futures, and a major equities downturn, it’s forgivable if people forget the precursors that lead to this financial crisis. The case in point being that the Fed injected massive amounts of money into what’s known as the “repo market”, which is composed of repurchase agreements for government securities. People lend these contracts overnight, investors purchase them and then these institutions buy them back the next day at a slightly higher price. It can be thought of as an overnight lending market. In order to understand what went wrong, let’s start with the basics of banking.

The business of banking is essentially to grow client deposits by lending those deposits out and then turning around and garnishing more deposits. Here’s how that works.

Imagine you’re a financial institution offering a competitive rate on deposits. As people continue to use your banking services because they like your rates, your deposit base grows in tandem. Eventually, you have enough money to lend out to other people, which is great because you’re getting paid interest on that money.

Eventually you lend out so much money that you no longer have enough deposits to continue that growth trajectory, so you need to increase your rates while remaining competitive with other banking services in the market. If you cannot grow your deposit base by bringing in more clients, you’ll be out of the banking business shortly. As one can imagine, this creates a vicious cycle [1].

Not all banks are at the same stage of the abovementioned cycle, so some institutions will have money to lend, while other banks have overnight obligations that they need to meet, and the latter borrows money from their peers. For an institution the size of JP Morgan or Wells Fargo, this is almost always in the form of Treasury securities (as they are seen as the most liquid), which they’ll buy back for an agreed-upon price the next day [2]. It’s basically an immediate access to liquidity, and this works because treasury securities are seen as highly liquid assets because they’re backed by the full faith and credit of the United States government.

It’s a win-win situation for the lender and the depositor. However, due to the size of many of these institutions, the Federal Reserve has imposed limits ($500 billion) on how much they can loan out in a given period. For example, and this number can fluctuate, let’s say the limit is $20 billion. JP Morgan or Wells Fargo can’t turn around and loan $100 billion for an overnight repo session — There are regulations in place which prevent one bank or group of banks from completely dominating the repo market.

Another way to make sure larger institutions don’t undercut smaller competitors is by setting a range at which these repo deposits can be lent. The limit is set at a fixed rate by the Federal Reserve, and at the beginning of september of 2019, that limit was 1.75%. The limit has since fluctuated between 1.5% and 2%, but ultimately what happened was a massive drawdown of available USD in the Repo market due to JP Morgan’s withdrawal of liquidity (more on that shortly). The Fed responded to the emergency by injecting money into the repo market in an effort to keep actual rates within their target range. Said another way, there simply weren’t enough dollars to go around for many financial institutions, and more importantly, for hedge funds.

When the top blew off the repo market

Hedge funds are key players in this discussion, as they utilize the repo market system to meet their overnight obligations, and this is a great deal of capital attached to not only the hedge funds, but all of the clients that they serve. A hedge fund may utilize the repo market to cover their business obligations overnight, as they are able to pay them back the next day by actualizing profits on a position. Hedge funds utilize this interbank repo market in the same way financial institutions such as banks do. Ultimately, the drawdown of dollars via institutions such as hedge funds borrowing in the repo market led to a bottom-up pressure effect similar to what happens when you shake a soda bottle — eventually the top blows off.

Jamie Dimon — head of JP Morgan — had an ingenious idea that worked extremely well, which was to withdraw a chunk of JP Morgan’s cash (57%) from the repo markets. Over the course of a couple months, JP Morgan withdrew nearly 160 billion dollars worth of liquidity that otherwise would have been served in the repo markets. This pulling of the rug led to enormous pressure on the repo market (in those institutions’ ability to loan and pay interest on overnight loans consistent with the Fed’s recommended rates).

When the cap burst off the repo market, the set Fed interest rate of 1.75% was rendered invalid, as the actual market rate for repo funds soared to 10%. Financial institutions such as banks and hedge funds were willing to pay 2.5%, 4%, 6% and beyond, even though that would accrue a penalty from the Federal Reserve. That escalated until the rate for overnight deposits loans until the Fed stepped in to put out the fire, and the simple solution for that was to (print and) inject money into the repo market in exchange for Treasuries, and those are called repo injections.

Let’s repeat that — repo injections were created by the Federal Reserve in the form of loaning Treasury securities. In order to ease pressure on repo markets, the Fed assured the world that they would remain the lender of last resort when other institutions failed to lend. The Federal Reserve’s “solution” seemed to work for a while.

The money needed to flow downstream, so JP Morgan bought various securities — equities, treasuries, bonds — an ingenious move to front-run and profit from the inevitable Fed intervention, or rather, the momentum created by actions of the Fed. When the Fed injected funds into the repo market, banks that were holding large security positions were in line to benefit. no one wants a bank failure. And what about those hedge funds from earlier? In recent years, and especially since the Great Recession, there has been a massive explosion in leveraged trading. Let’s connect those dots.

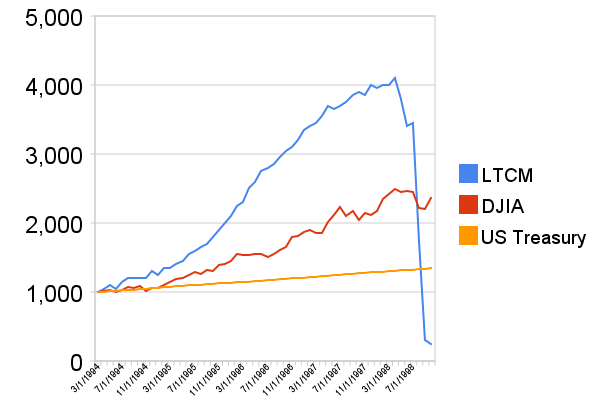

Long-Term Capital Management (LTCM) was a hedge fund that operated back in 1998 that became over-leveraged in equity positions to the point that it threatened a wave of cascading defaults in equity markets. LTCM suffered a sudden and intense downturn in the vast majority of their leveraged positions, which would have caused a cascade of defaults and micro-crash in the market had the Fed not back-stopped those positions on their behalf. It was one of the first times the Federal Reserve directly bailed out a hedge fund, and in this case a fund that was going under due to reckless and (ironically) unhedged behavior.

Who stood to benefit from this emergency?

That was not something the Federal Reserve was willing to let happen, therefore they opted to inject cash into the repo system. Meanwhile, JP Morgan purchased equities with cash that they otherwise would have used in the repo market. Without surprise, equity prices began to climb; it turns out when the Fed indirectly back-stops hedge fund equity positions, the market responds very positively. JP Morgan forced the Fed’s hand by pulling cash out of the market — The Fed had no choice but to inject cash themselves. This resulted in heavy profit for the company and their shareholders. Remember, hedge funds can invest in equities, so when JP Morgan forced the Fed to pick up the slack, this in turn drove up equity prices. It was an ingenious move by JP Morgan.

What that ultimately did is what the financial system in its current iteration seems to do best — with the Federal Reserve at the helm, Main Street suffers while Wall Street becomes ever-wealthier through the virtues of money printing. This ultimately leads to consumer price inflation and higher equity prices, ensuring the investment game will be ever harder for the little guy. This system produces massive inequality as a result of consistent (and often unnecessary) market intervention.

Individuals or firms that already owned disproportionate amounts of equity were set to benefit tremendously from the Fed’s actions in the repo market, and many keen leaders understood the implications of this precedent in money lending and printing.

In summary, it was a major payday for a few people. Not only were they able to withdraw cash positions, but they were able to inject that cash into equities on the back of the Federal Reserve’s actions. This means the Fed supported not only banks and their equity positions, but also the hedge funds. JP Morgan was able to use these highly leveraged hedge funds as a tool to force the hand of the Fed and get them to print more money.

That’s the story of the repo market.

Fast-forward to the present and we are in an environment in which The Federal Reserve has kept rates low for so long that they now face multiple LTCM situations in the form of highly leveraged hedge funds. The Fed is facing an avalanche of defaults if hedge funds aren’t able to get the liquidity they need to maintain their leveraged positions and (hopefully) slowly wind those positions down. The result would be a crash in equity markets the world over, but in today’s accommodative environment, why would these funds bother to reduce their positions in the first place?

Footnotes

[1] Of course, banking isn’t that simple. Economist Hyman Minsky once said, “Banking is not money lending; to lend, a money lender must have money. The fundamental activity is accepting, that is, guaranteeing that some party is credit worthy. A bank, by accepting a debt instrument, agrees to make specified payments if the debtor will not or cannot.” (Source: https://nathantankus.substack.com/p/banks-as-debt-monetizers-monetary)

[2] Central banks don’t usually participate directly in the repo markets but rather set the repo market rate. Large banks that participate include JP Morgan, Wells Fargo, and other GIS banks.