How much to raise is both an art and a science, a topic discussed at length in many other posts. What this article will focus on are the reasons specifically an entrepreneur similar to you might be raising more money. It’s really a function of five factors: stage, geography, investors, credibility, and strategy.

1) Stage — The amount of money raised is not what defines the stage of a company, it’s what you use the money for. Frameworks are imperfect but useful guidelines and the one below is what we believe in at Tau Ventures. Later stage implies raising more at a higher valuation.

| Stage | What You Are Proving | Typical Dilution |

|---|---|---|

| pre seed | powerpoint | 10-20% (*) |

| seed | prototype | 20-30% (*) |

| series A | product-market fit | 20-30% (**) |

| series B | business model taking off | 15-20% |

| series C and beyond | scaling / growth including acquisitions | 10-15% |

(*) or equivalent if you doing a convertible

(**) if you previously did convertibles this is typically when they convert

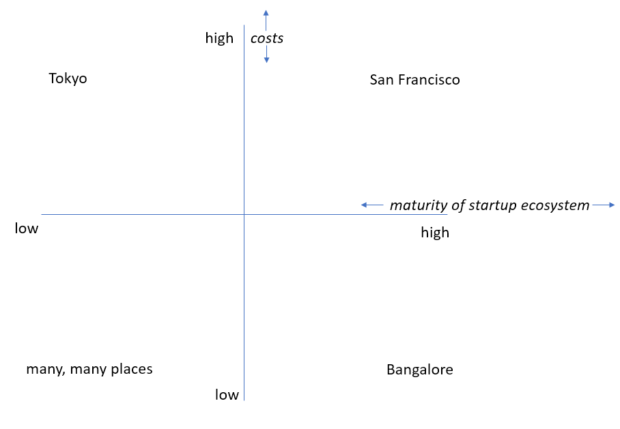

2) Geography — The world is definitely not flat. The 2×2 matrix below is another framework to consider, with some representative cities listed. The higher you are on both axes the larger the rounds will be.

3) Investors — “Institutional investors” is the catch all for traditional, financially-motivated VCs.The framework below is a practical way of understanding the lens of each investor and thus the amount and valuation they would consider investing:

| Stage | What The VC Is Hoping | Expectation Around Exit |

|---|---|---|

| pre seed | 10x+ | 10+ years |

| seed | 10x | 10 years |

| series A | 5x | 7-8 years |

| series B | 3-4x | 4-5 years |

| series C and beyond | 2-3x | 2-3 years |

Huge caveat around the exit expectation — funds can exit earlier by selling to other funds. For instance, in practice a seed investor will do a secondary (ie sell their ownership to another investor, typically a larger one) between years 4-7 when the startup has hit series B and the fund has achieved already a 5x.

Funds looking to establish themselves will often pay up more. Foreign funds will often fall under this category. Strategic investors typically follow rather than lead the rounds but when they do set the terms, they often span a wider spectrum in terms of amount / valuation than purely financially motivated investors.

4) Credibility — All things equal, two startups may still raise vastly different amounts based on the entrepreneur. Three main factors to consider are the entrepreneur’s

- work experience

- history of exits

- relationship with the investors

You may ask — some difference in amounts / valuations is understandable but how is orders of magnitude justifiable? Venture capital is based on power laws ie a few startups succeed hugely. So the belief is that betting disproportionately on an entrepreneur who is more experienced, with more exits, who the VCs already know well, is actually much lower risk.

5) Strategy — Finally, an entrepreneur may simply be building a more capital-intensive model or and/or be willing to put up with more dilution. Consider two competitors at the seed stage, one raising $1M at a post of $5M, the other $3M at a post of $10M. The first one is diluting only 20% and presumably keeping a monthly burn of ~$100K to last 12 months. The second one is diluting 33% and presumably keeping a monthly burn of ~$250K to last 24 months. Since valuations and burn rates are rarely disclosed publicly, just based on the amount raised it may look like the second entrepreneur has the upper hand — which is not the full story.

Originally published on “Data Driven Investor,” am happy to syndicate on other platforms. I am the Managing Partner and Cofounder of Tau Ventures with 20 years in Silicon Valley across corporates, own startup, and VC funds. These are purposely short articles focused on practical insights (I call it gl;dr — good length; did read). Many of my writings are at https://www.linkedin.com/in/amgarg/detail/recent-activity/posts and I would be stoked if they get people interested enough in a topic to explore in further depth. If this article had useful insights for you comment away and/or give a like on the article and on the Tau Ventures’ LinkedIn page, with due thanks for supporting our work. All opinions expressed here are my own.