Quality Data, Quality Decisions: Why Web Scraping is Essential for Advanced Analytics

Gediminas Rickevičius·9 min

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

from statsmodels.tools.eval_measures import rmse

import seaborn as sns

import statsmodels.api as sm

import itertools

from statsmodels.tsa.arima_model import ARIMA, ARMA

import warnings

warnings.filterwarnings("ignore")

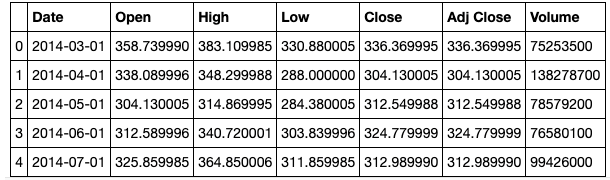

Now it’s time to import the dataset and view it. We do so using the panda's library and its read_csv function.

data = pd.read_csv('filepath')

data.head()

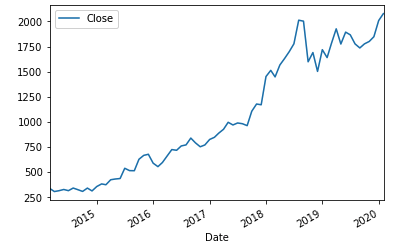

We are only interested in the “Close” price. Also, we need to set the date as the index for the data frame.

We are only interested in the “Close” price. Also, we need to set the date as the index for the data frame.

df = data[['Date','Close']]

df.Date = pd.to_datetime(df.Date)

df = df.set_index("Date")

Now that we have preprocessed our data, we can view the data as a line plot. Visualising our data is an important part of exploratory data analysis.

df.plot(style="-")

When fitting an ARIMA model, we aim to find the values of our parameters p,d and q which optimise or minimise a certain metric of interest. There are many methods to achieve this goal and yet the correct parametrization of ARIMA models can be a tedious process that requires statistical expertise and time. In this tutorial, we hope to overcome this issue by writing a grid search algorithm in python to select the optimal parameter values for our ARIMA(p,d,q) time series model.

The use of a “grid search” is to iteratively explore different combinations of parameters. For each combination of parameters, we fit an ARIMA model with the SARIMAX() function and assess its overall performance. Once we have explored the entire domain of parameters, our optimal set of parameters will be the one that yields the best performance for our criteria of interest. In this scenario, our criteria of interest is the Akaike information criterion (AIC). The AIC measures how well a model fits the data while taking into account the overall complexity of the model. We are therefore interested in finding a model that returns the lowest AIC value.

In the code below we define the parameters and generate all possible combinations of the parameters.

When fitting an ARIMA model, we aim to find the values of our parameters p,d and q which optimise or minimise a certain metric of interest. There are many methods to achieve this goal and yet the correct parametrization of ARIMA models can be a tedious process that requires statistical expertise and time. In this tutorial, we hope to overcome this issue by writing a grid search algorithm in python to select the optimal parameter values for our ARIMA(p,d,q) time series model.

The use of a “grid search” is to iteratively explore different combinations of parameters. For each combination of parameters, we fit an ARIMA model with the SARIMAX() function and assess its overall performance. Once we have explored the entire domain of parameters, our optimal set of parameters will be the one that yields the best performance for our criteria of interest. In this scenario, our criteria of interest is the Akaike information criterion (AIC). The AIC measures how well a model fits the data while taking into account the overall complexity of the model. We are therefore interested in finding a model that returns the lowest AIC value.

In the code below we define the parameters and generate all possible combinations of the parameters.

# Define the p, d and q parameters to take any value between 0 and 3 p = d = q = range(0, 3) # Generate all different combinations of p, q and q pdq = list(itertools.product(p, d, q))In the next few lines of code, the SARIMAX() function is applied to all combinations of parameters and the model with the lowest AIC is printed.

warnings.filterwarnings("ignore")

aic= []

parameters = []

for param in pdq:

#for param in pdq:

try:

mod = sm.tsa.statespace.SARIMAX(df, order=param,

enforce_stationarity=True, enforce_invertibility=True)

results = mod.fit()

# save results in lists

aic.append(results.aic)

parameters.append(param)

#seasonal_param.append(param_seasonal)

print('ARIMA{} - AIC:{}'.format(param, results.aic))

except:

continue

# find lowest aic

index_min = min(range(len(aic)), key=aic.__getitem__)

print('The optimal model is: ARIMA{} -AIC{}'.format(parameters[index_min], aic[index_min]))

The output is: The optimal model is: ARIMA(0, 2, 1) — AIC:853.8946396688659

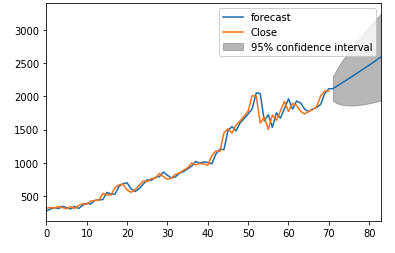

The next step is to fit the ARIMA(0,2,1) model to our time series.

model = ARIMA(df, order=parameters[index_min]) model_fit = model.fit(disp=0) print(model_fit.summary())Finally, we can forecast the next 12 months and visualise the data points thereafter.

model_fit.plot_predict(start=2, end=len(df)+12) plt.show()

There we have it! Your first stock prediction algorithm. However, please note that it is extremely difficult to “time” the market and accurately forecast stock prices. This tutorial should not be seen as trading advice and the purchasing/selling of stocks is done at your own risk.

There we have it! Your first stock prediction algorithm. However, please note that it is extremely difficult to “time” the market and accurately forecast stock prices. This tutorial should not be seen as trading advice and the purchasing/selling of stocks is done at your own risk.As a current Masters in Statistics student, Luka is eager to simplify complex topics and provide big-data solutions to real-world problems. He also has an educational background in actuarial and financial engineering. In his spare time, Luka enjoys traveling, writing on machine learning topics and taking part in data science competitions.