Synopsis: Following the 2008 financial crisis, Central Banks around the world responded aggressively, cutting interest rates significantly (500 bps by the FED) and in some cases, into negative territory (-0.40% for the ECB). This loss-limiting response placed downward pressure on forward interest rates (Figure 1) and the yield curve (Figure 2). Nevertheless, Central Banks’ inflation targeting, anchored inflation expectations and continued demand for safe assets also explain the trend of falling forward rates and expected returns.

Ten years after the financial crisis, quantitative easing (QE) has supported economic growth and stopped deflationary pressures that were a worrisome trend in most advanced economies. As Central Banks bought large portions of corporate and public sector debt, forward interest rates fell more noticeably. This worrying trend can, however, also be attributed to confidence in a monetary policy designed to achieve the inflation target at any cost, it seems.

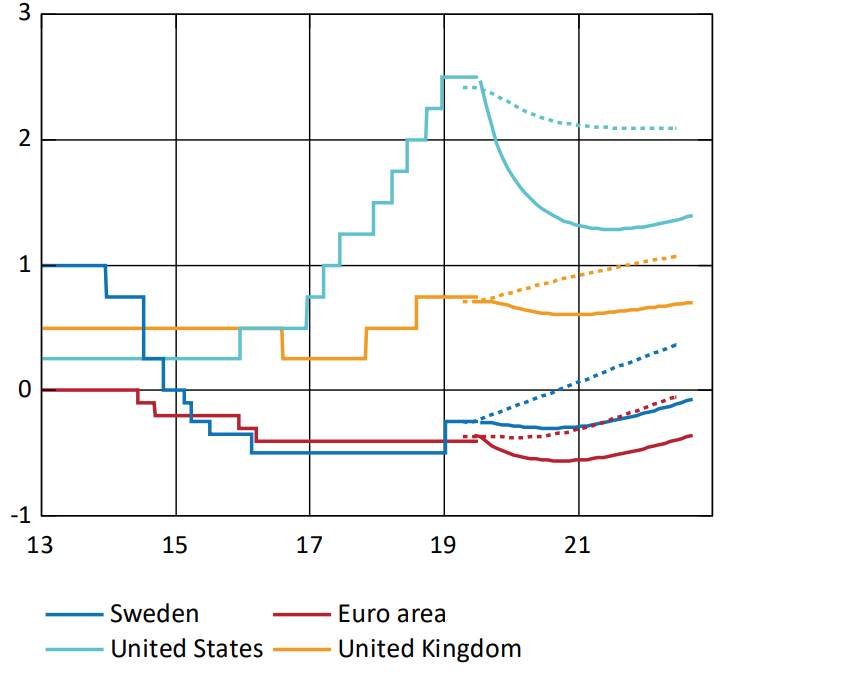

Figure 1: Forward rates are lower than previously forecasts by Major Central banks (%)

QE – life with less life support

As a result, bond yields remain negative in most countries as investors hold the asset as a hedge during more volatile times in the stock market, and, to ensure liquidity during a downturn. This is especially true for assets that are susceptible to distortions in the labor market and household consumption. The 2008 financial crisis saw liquidity dry up as asset prices tumbled. This twin shocks to financial markets justified QE as it not only prevented a more marked fall in asset prices and inflation but also provided liquidity for illiquid markets.

Signals, transmission channels

If QE is designed to communicate continued dovishness and isn’t responsible for the shape of the yield curve and falling forward rates as illustrated in the chart above, what might be? The inflation rate and real rate plausibly do. The relationship between assets and consumption and/or an upside surprise to inflation will cause investors to demand a risk premium to compensate for lower rates of returns. This was unlikely to happen following the financial crisis as our commodity-centric inflation targeting suggests the risks of upside remain unlikely. It seems 2.0% inflation is now contingent on geopolitical tensions, procyclical fiscal stimulus as record Central stimulus has done all but achieve the inflation target. As Gertan Vileghe argues here, we would need to see a sustained increase in the term premium only if we see a change in risk fundamentals. A shock-induced divergence of inflation outcomes from Central Bank forecasts is, therefore, the only driver of such an outcome.

Figure 2: Longterm rates have been trending down steadily since 1989 (%)

The reason lower forward rates cannot, in isolation, be attributed to QE as the latter works via similar mechanisms to changes in the official policy rate. Both QE and policy rates work via open market operations, the former works via short-term interest rates (SONIA) and QE works via money supply and the creation of Central Bank reserves. As such, QE only serves to emphasize Central bank dovishness and forward guidance.

Nevertheless, both QE and policy are designed to achieve the inflation target; changes to interest rates seeks to guide expectations of future monetary policy; not only does QE provides greater clarity on future policy, it also effectively communicates the Central Bank’s response function, which is unlikely when interest rates are low or in negative territory. This is particularly evident following a downturn when the transmission mechanisms from negative interest rates are noisy and the expectations channel (future path of monetary policy) needs to be guided more closely to prevent inflation expectations from de-anchoring from the 2.0% target.

How unlikely is this?

It is incomplete to judge the effectiveness of QE by looking at whether or not the inflation target has been achieved. Rather, a more complete picture will look at the behavior of inflation following the crisis, with the nature of relationships such s the Philips curve or the Taylor rule. Inflation trended upwards in 2016, recovering some lost ground but steadily declined in recent months despite geopolitical uncertainty, rising crude production and waning of the U.S fiscal stimulus. As such, whilst a supply shock could drive prices higher, it remains a remote prospect. More worrying though, is the fact that inflation is certainly depressed by global factors such as technological progress and the internet of things, resulting in price-limiting competition. This is why record low unemployment in the United States has seen underlying inflation at 1.8% whilst the headline figure fell well below the FED’s 2.0% target. Meanwhile, underlying inflationary pressures are most certainly present in Britain, but inflation has also been supported by a weaker pound — following Brexit and higher business overheads.

Can inflation consistently return to the 2.0% target

It is difficult to see inflation returning to the 2.0% target consistently without structural changes as rising global crude supply and unresponsive tightness from labor markets appear to become the norm. Even as real incomes have risen somewhat, they remain well below the inflation target, with weaker currencies reduce consumer purchasing power. This, in turn, negates any benefits that could accrue by way of higher prices — prompted by demand pressures.

As such, one could argue that quantitative easing has provided liquidity, supported the economic recovery and inflation despite the latter failing to rise to 2.0% consistently. More importantly, it has extended the financial and economic cycle — essentially lessening the fallout from the 2008 crisis raising our tolerance for leverage and extending debt maturities.

QE and its effects!

It will be unwise and incomplete to criticize QE for its distortive effects whilst understating liquidity and prevention of unemployment and a more marked correction in asset prices. Nevertheless, whilst QE increased liquidity and signaled an accommodative stance for the foreseeable future, one cannot say with certainty that financial flows shifted into riskier assets and the real economy as traditional mechanisms of QE will suggest. This explains the lackluster recovery following the financial crisis and the need for fiscal stimulus in the U.S. to ensure a global cyclical upswing in 2018. As I argued here, QE is a loss-minimizing mechanism at best, which will explain years of austerity and pro-cyclical stimulus in some countries to lift economic activity.

If investors didn’t redirect finance into capital investments and human capital, then the transmission mechanism from riskier assets to the real economy is less palpable or the bond bias never left! The latter is not unlikely as continued bond issuance either suggest a precarious macroeconomic backdrop or a more debt-dependent economic and financial cycle. It is not premature to overstate levels of public and private sector debt as record-low interest rates and falling forward rates provide a greater buffer against a credit-induced shock just yet. As firms and household balance sheet dictate the passthrough of policy rates, expectations of future monetary policy and firmly anchored inflation expectations also explain falling forward rates.