We live in interesting times - a crossroads where four generations make up the changing demographics of the evolving global economy. This has not only given rise to the new tech- enabled model of the Gig Economy, but has brought forth varying styles of investing that Baby Boomers, Generation X, Millennials & Generation Z bring to the table. The stark difference between the risk profiles of Baby boomers, most of whom are on their way to retirement compared to Gen Z, who are beginning to enter the workforce gives rise to different styles of investing.

Investing is easier said than done and takes a little more planning & acumen. Depending on your knowledge of Investing, you have a choice of a self-directed or a managed account. The former is only suggested if you have advanced knowledge of the subject & more importantly have the time to manage your account on a consistent basis. However, if you are like the majority, where you are either not from a financial background or simply don’t have the time then you should opt for a good financial adviser who can understand your risk profile, objectives & goals to build a suitable portfolio matching these metrics.

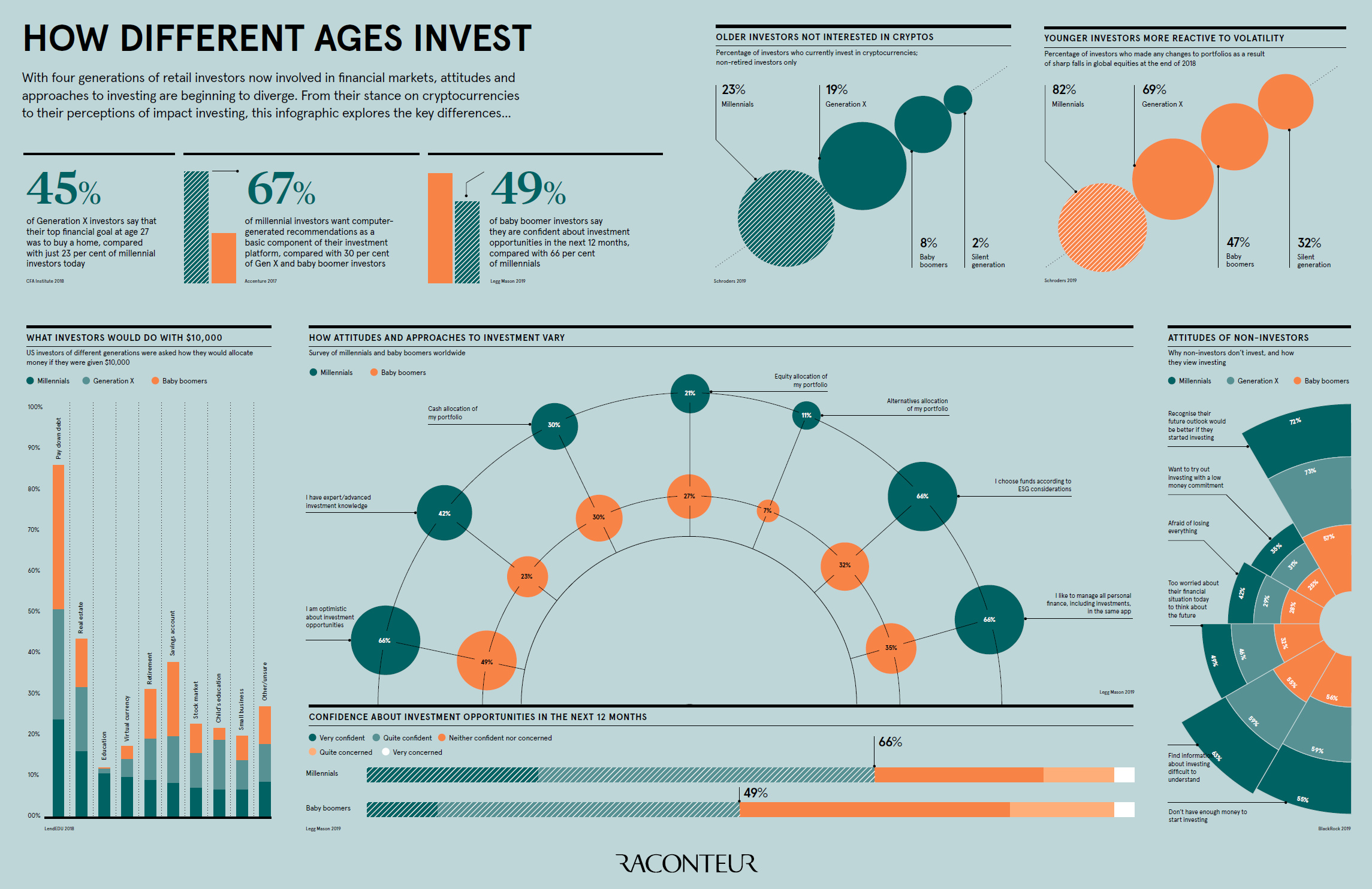

The data above highlights some of the differences in investing styles among the four generations that I was talking about earlier. Investing differs mainly depending on which age group you belong to, but there are other external factors like geopolitical conditions, economic cycles & the cultural impact. Let's comb the data from presented in the infographic to get some further insights. The infographic from Raconteur makes reference to the silent generation rather than Generation Z. Frankly, I had no clue myself that a demographic like the 'silent generation' existed - apparently refers to the people born between 1925-1945, and labelled as such since people who grew up in this era worked very hard & kept quiet.

Anyways, coming back to the Investment objectives & styles, following observations were made in this study:

- Different Financial Goals - 45% of the Generation X said their top priority was to buy a house. This figure dropped to almost half or 23% only when it came to Millennials. Investment in Property is obviously on a declining trend with the newer generations.

- Future Prospects - Almost two-thirds or 66% of the Millennials were confident about investment opportunities in the next 12 months as compared to only 49% of the baby boomers. The optimism is evident in the younger generation in this segment.

- Tech-savvy - Similarly, 67% of the Millennial investors wanted some automation as part of their investment platform. Gen X & baby boomers are much less forthcoming in this regard with only 30% of them comfortable with computer-generated investment solutions.

- Cryptos investment - As expected Millennials were the biggest investors in the digital assets with 23% currently owning them while 8% baby boomers & 2% silent generation invested in them. The younger generation is more receptive to the idea of investing in the emerging digital model.

- Volatility Response - The younger Millennials with 82% were much more proactive in adjusting their investment portfolios in response to sharp falls in Equities as the one we saw at the end of 2018. They were followed by 69% by Gen X and 47% Baby boomers.

- Investment Management - 66% of the Millennial investors liked the idea of everything under one roof idea to manage personal finance, including personal investment as being important. Almost half (35%) of baby boomers agreed. Goes to show the younger generation is much more comfortable with the use of technology for their financial needs.

- Impact Investing - Investing having a positive impact on the society with ESG (environmental, social, and governance) investing model was on the minds of two-thirds of the Millennials, while only 32% of the baby boomers considered this to be of important to them.

- NOT Investing - While almost three-fourths of Millennials & GenX and 57% Boomers thought of investment improving the personal future outlook, all of them considered difficulty in learning investment concepts & not having enough funds to invest being the two major hindrances to start investing.

By and large, the analysis suggests that the younger generation is much more tech-savvy, dynamic, socially conscious with a different set of financial goals than the predecessors. Times are changing...

Email ?|

Twitter ?

| LinkedIn ?

| StockTwits ?

| Telegram ?