Giant Trading Losses – What not to do? <a>Chapter 3 – The widow maker arbitrage on Natural Gas / Amaranth Advisors</a>

Veerasenthil Athiban·8 min

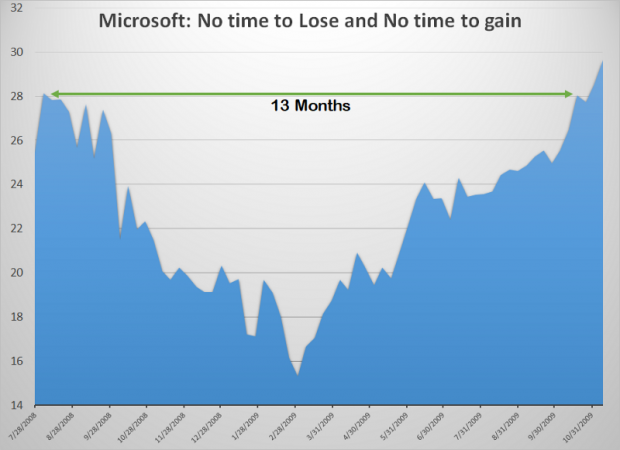

Chart created by Author: Data Source Yahoo Finance MSFT[/caption]

Microsoft’s quarterly revenue growth during this period was 9.44%, 1.60%, -5.58% and -14.22%. Its worst quarterly performance came right before Microsoft regained its pre-financial crisis pricing. It’s clear that Microsoft’s business earnings and revenue growth had nothing to do with its 2009 market valuation.

If you had bought a single unit of SPY, an ETF that tracks the S&P 500 index, in February 2008 and held it till April 17th, 2020, you will be sitting on a return of 275.75%.

Chart created by Author: Data Source Yahoo Finance MSFT[/caption]

Microsoft’s quarterly revenue growth during this period was 9.44%, 1.60%, -5.58% and -14.22%. Its worst quarterly performance came right before Microsoft regained its pre-financial crisis pricing. It’s clear that Microsoft’s business earnings and revenue growth had nothing to do with its 2009 market valuation.

If you had bought a single unit of SPY, an ETF that tracks the S&P 500 index, in February 2008 and held it till April 17th, 2020, you will be sitting on a return of 275.75%.

Decision Paralysis is a clear and present danger to investing. “Research shows that if you’re surrounded by an abundance of options, you typically end up less satisfied with your final decision than if you’d been given fewer options in the first place,” says Psychologist Eva M. Krockow Ph.D. Do yourself a favor and always keep a list of, preferably a handful, investment ideas ready.

Complicating is easy, keeping it simple is the hard part.

Decision Paralysis is a clear and present danger to investing. “Research shows that if you’re surrounded by an abundance of options, you typically end up less satisfied with your final decision than if you’d been given fewer options in the first place,” says Psychologist Eva M. Krockow Ph.D. Do yourself a favor and always keep a list of, preferably a handful, investment ideas ready.

Complicating is easy, keeping it simple is the hard part.

Hedging costs money but so does car insurance premiums. Will you drive your car without insurance? You compare insurance providers, check their quotes, negotiate a better deal if possible. But at the end of it all, you pay the premium year after year. You never saw that as an unnecessary expense.

Our investment portfolio is worth a lot more than our car, but we rarely think about buying insurance.

Hedging - Example: Let us assume that I am ready to invest $30,000 and I think there is a good chance that the economy might face a severe, prolonged downturn. I am also worried that the market will keep going up in the short term and I will lose a great entry point. I am kind of confused as I am thinking in all directions.

But I have decided to dip my toe anyway and create the following plan:

Hedging costs money but so does car insurance premiums. Will you drive your car without insurance? You compare insurance providers, check their quotes, negotiate a better deal if possible. But at the end of it all, you pay the premium year after year. You never saw that as an unnecessary expense.

Our investment portfolio is worth a lot more than our car, but we rarely think about buying insurance.

Hedging - Example: Let us assume that I am ready to invest $30,000 and I think there is a good chance that the economy might face a severe, prolonged downturn. I am also worried that the market will keep going up in the short term and I will lose a great entry point. I am kind of confused as I am thinking in all directions.

But I have decided to dip my toe anyway and create the following plan:

Resultant Scenarios: Six Months later

When the hedge expires in November, my portfolio value would have changed as follows.

Resultant Scenarios: Six Months later

When the hedge expires in November, my portfolio value would have changed as follows.

The hedge would have taken a good bite of my profits had the market moved higher. But my portfolio would have lost just 3% if the market declined by more than 45%. Hedging would have done what it was supposed to: make sure that I don’t collect outsized losses when the market goes crazy on the downside.

Note: I have not included commissions as part of the calculations. SPY ETF does not accurately track the S&P 500 index. If you are comfortable with options, you can consider a bear put spread to reduce the cost of your hedge.

The hedge would have taken a good bite of my profits had the market moved higher. But my portfolio would have lost just 3% if the market declined by more than 45%. Hedging would have done what it was supposed to: make sure that I don’t collect outsized losses when the market goes crazy on the downside.

Note: I have not included commissions as part of the calculations. SPY ETF does not accurately track the S&P 500 index. If you are comfortable with options, you can consider a bear put spread to reduce the cost of your hedge.

Make sure that you keep a high degree of threshold on any company that enters this list, the harder your selection criteria the better. I recommend placing only companies with a net cash position on this list because companies with no debt don’t go bankrupt.

Fast Growers: Small companies with an aggressive growth rate.

Cyclicals: Companies in cyclical industries such as airlines and auto. Both these industries are well known for the boom-bust cycle.

Asset Plays: These are companies that trade far below their value, making them an attractive bet for investors. According to Peter Lynch, this could be “any company that’s sitting on something valuable that you know about, but that the Wall Street crowd has overlooked.”

Turnarounds: Companies that are barely surviving. But if they turn things around and fix the problems they are facing, the stock price will rebound.

Portfolio Insurance: Bear markets tend to be short-lived and you need insurance only when you are anticipating a bear market. According to Invesco, the average length of bull markets since 1956 is 55.1 months. The average length of a bear market is just 11.7 months. If you are investing since 1956, you would have bought insurance for your portfolio less than 18% of the time.

Key Points to Remember: Some companies will qualify to be in multiple categories. But if you know why you are making the purchase, you will place them in the right category. Once they are positioned in the right place, it will be easy for you to decide when to sell and when not to sell the position. When fundamentals change, companies must be repositioned to the respective category, forcing you to automatically change your expectations.

Category Rebalancing - Example: Let’s assume that I have bought shares in Apple and Google. I place them under the Stalwarts section as the odds of both the companies going bankrupt is extremely low. Ten years after I purchased them, a new management team decides to binge on debt and both companies drift quickly towards net debt. I will now remove them from Stalwarts and place them under the Slow growers.

Re-balancing a portfolio is easier with categories than without it. During a recession, I will be least worried about the companies that I placed under Stalwarts. I will exit turnarounds and asset plays, question my cyclical positions and take a real close look at companies placed under slow growers.

Investing is not rocket science. To be successful you need knowledge of simple math, a small dose of common sense, a decent amount of discipline, and an ability to accept mistakes. Things, a lot of us have. But somehow we have all managed to make it appear more difficult than it actually is. If you can break the complexity down and set the terms of your engagement, you will start off from a favorable position.

Make sure that you are the one who dictates the terms of your portfolio, not the stock’s current price.

Make sure that you keep a high degree of threshold on any company that enters this list, the harder your selection criteria the better. I recommend placing only companies with a net cash position on this list because companies with no debt don’t go bankrupt.

Fast Growers: Small companies with an aggressive growth rate.

Cyclicals: Companies in cyclical industries such as airlines and auto. Both these industries are well known for the boom-bust cycle.

Asset Plays: These are companies that trade far below their value, making them an attractive bet for investors. According to Peter Lynch, this could be “any company that’s sitting on something valuable that you know about, but that the Wall Street crowd has overlooked.”

Turnarounds: Companies that are barely surviving. But if they turn things around and fix the problems they are facing, the stock price will rebound.

Portfolio Insurance: Bear markets tend to be short-lived and you need insurance only when you are anticipating a bear market. According to Invesco, the average length of bull markets since 1956 is 55.1 months. The average length of a bear market is just 11.7 months. If you are investing since 1956, you would have bought insurance for your portfolio less than 18% of the time.

Key Points to Remember: Some companies will qualify to be in multiple categories. But if you know why you are making the purchase, you will place them in the right category. Once they are positioned in the right place, it will be easy for you to decide when to sell and when not to sell the position. When fundamentals change, companies must be repositioned to the respective category, forcing you to automatically change your expectations.

Category Rebalancing - Example: Let’s assume that I have bought shares in Apple and Google. I place them under the Stalwarts section as the odds of both the companies going bankrupt is extremely low. Ten years after I purchased them, a new management team decides to binge on debt and both companies drift quickly towards net debt. I will now remove them from Stalwarts and place them under the Slow growers.

Re-balancing a portfolio is easier with categories than without it. During a recession, I will be least worried about the companies that I placed under Stalwarts. I will exit turnarounds and asset plays, question my cyclical positions and take a real close look at companies placed under slow growers.

Investing is not rocket science. To be successful you need knowledge of simple math, a small dose of common sense, a decent amount of discipline, and an ability to accept mistakes. Things, a lot of us have. But somehow we have all managed to make it appear more difficult than it actually is. If you can break the complexity down and set the terms of your engagement, you will start off from a favorable position.

Make sure that you are the one who dictates the terms of your portfolio, not the stock’s current price.Real-time institutional flow data and trading signals for serious investors.

Explore DataDrivenAlpha →Instantly repurpose any DDI article into a professionally produced short-form video.

Try DDI Media →Shankar Narayan is an MBA graduate from Kent State University with a passion for investing and technology. He works as an independent consultant and a freelance writer.