Synopsis: Debt levels in the public sector have been on an uptrend since the GFC, matching the trend seen in most advanced economies. Nevertheless, the statistic in isolation paints an incomplete picture. Recently enacted labor market reforms and a renewed focus on an innovation-driven model to growth suggests risks are tilted to the upside. Furthermore, these could also be the precursor to higher wages and recovery in productivity. Should upside risks materialize, the potential growth rate could negate the impacts of rising debt levels further.

France public debt has risen substantially following the 2008 GFC with the fiscal deficit breaching the EU’s key 3.0% level. The economy has, however, grown steadily supported by recent labor market reforms. Although it might too early to determine the impact of labor market reforms, rising employment in knowledge-intensive sectors suggests a net positive effect on the economy. The latter supported by a renewed focus on innovation-driven growth. As such, rising debt levels appear overstated as risks are tilted to the upside, absent external global shocks.

Public debt is back on the agenda.

Public debt levels are becoming increasingly important in developed markets; having grown steadily in France in the last decade, with a downtrend emerging in 2017. Furthermore, the economy was poised to exit the excessive deficit procedure prior to the “Yellow vest” protests. As such freezing fuel duties and income giveaways will push the deficit well above the EU’s key 3.0% target. The impact of debt levels is heterogenous compared to Italy owing to differing economic characteristics and banking structures. I caution against over pessimism on the Euro as a result.

Meanwhile, government debt to GDP ratio in the Euro area is 85.1% on average, markedly lower than that of France slightly below 100%. If France were to enter an excessive deficit procedure, yield spreads are unlikely to react significantly as a result as the EC spring forecasts currently forecast the deficit at 2.2% in 2020, together with more upbeat and intentional innovation policy, downside risks appear overstated.

It is premature to overstate the impact of rising debt levels on the French economy as the structural drivers of growth remain stable, supported by rising innovation. Furthermore, global policy and trade uncertainty has caused Central Banks to turn increasingly dovish, with the ECB reiterating its commitment to the inflation-driven monetary policy. Accommodative monetary policy bodes well for French public finances as a risk premium will, if at all, be based on financial conditions.

The French economy… Still “En Marche”

The French economy has been growing at a steady rate in the last decade, the five-year and 3-year average currently stands at 1.5% and 1.6% respectively. The European Commission currently forecast 1.5% growth for 2020 from 1.3% for end-2019. Despite idiosyncratic outcomes following the 2008 financial crisis, corporate investment recovered and grew more markedly in the previous two years. This negated the impact of falling government contribution to Gross fixed capital formation. Meanwhile, the household continues to spend, supported by a tighter labor market, with unemployment falling to 9.05% from 10% prior to the labor market reforms. Lackluster real income growth exacerbated by a proposed increase in fuel duties brought the French economy to a halt via social unrest.

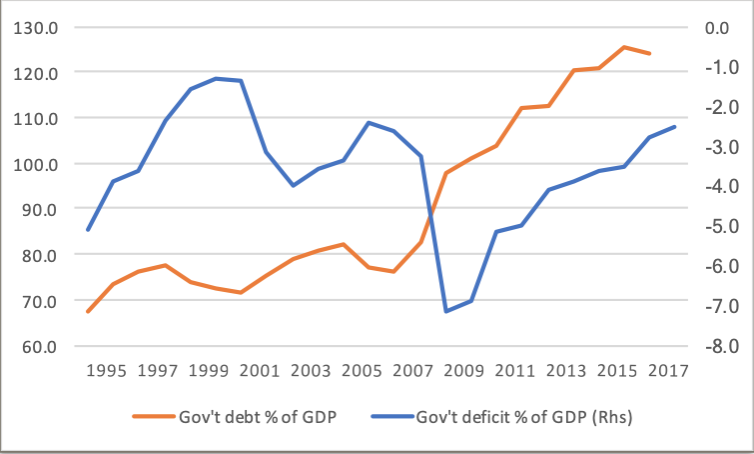

Rising debt levels paint an incomplete picture

Admittedly, rising debt levels are driven tax breaks and lower government revenues following the “Gillet Jaune” protests. Limited fiscal space could lessen the government’s ability to respond to a future downturn. Even so, debt sustainability is a remote prospect at this juncture. Little is, however, said about the growth effects from innovation gains. particularly, its ability to boost productivity, firm competitiveness and the potential growth rate. France is a strong economy, whose performance has increased relative to the EU as illustrated in the chart.

Innovation set to support the countries growth infrastructure

Innovation set to support the countries growth infrastructure

As the Eurozone’s second largest economy, France is transitioning to high-tech manufacturing and services. Its approach to innovation has followed this trend rather closely. R&D expenditure supported by venture capital, the public sector and businesses have focused on knowledge-intensive sectors. Although patents as a proxy for innovation paint an incomplete picture, they nevertheless provide a useful gauge for innovation. As illustrated in the chart below, patent applications have closely followed real GDP growth. My model finds a marginal, yet positive impact on GDP at 0.0004%.

While it might be somewhat challenging to disentangle the growth effects of patents and process-driven innovation, the growing share of employment in medium and high-tech manufacturing, as well as knowledge-intensive sectors, provide clearer signals for productivity and a potentially higher growth rate.

My model finds a unit increase in labor productivity and utilization boost real GDP by 1.04%. This supports the view that process innovations, as illustrated by a rising share of knowledge-intensive employment suggest a noticeable level of diffusion from innovation to the economy.

It is, therefore, important to discuss rising debt levels with the potential upside risks to GDP growth and productivity from technological advancements. This trend is further emphasized by the recently enacted labor market reforms, designed to up-skill the labor force as well as lessen rigidity for both employees and employers. Absent a pronounced shock to the global economy, reforms and a growth-centric approach to innovation suggest upside risks for growth in the coming years.

Market implications.

A higher potential growth rate will likely de-anchor the Euro from more global drivers with a recovery in productivity likely to precede higher growth levels. Bond yields are unlikely to widen significantly as a result of a more upbeat economic backdrop. As such, labor market reforms and an innovation-driven model suggests risks are tilted to the upside.