Gold, Silver, Platinum, Palladium, Rhodium: Each Precious Metal Is Precious in Its Own Unique Way

Olegs Jemeljanovs, PhD, CFA·7 min

The majority of posts included words like “love” and very few expressed anger or disappointment.

As a point of comparison, luxury fitness brand Equinox inspired mixed feelings over the last three months:

The majority of posts included words like “love” and very few expressed anger or disappointment.

As a point of comparison, luxury fitness brand Equinox inspired mixed feelings over the last three months:

Many users included angry language in their posts in response to Equinox’s chairman hosting a lavish fundraiser for Donald Trump, which led to calls for a boycott of the company’s luxury gyms.

The fact that people like Peloton as a brand really matters. There are only so many $2,000 bikes they are going to be able to sell. The secret to their long term success will be to keep subscribers to their digital content, so that each new customer they secure continues to contribute revenue to the company over time.

So the “selling happiness” thing is actually really important - if their customers stay happy, then their long term revenues are secure.

Many users included angry language in their posts in response to Equinox’s chairman hosting a lavish fundraiser for Donald Trump, which led to calls for a boycott of the company’s luxury gyms.

The fact that people like Peloton as a brand really matters. There are only so many $2,000 bikes they are going to be able to sell. The secret to their long term success will be to keep subscribers to their digital content, so that each new customer they secure continues to contribute revenue to the company over time.

So the “selling happiness” thing is actually really important - if their customers stay happy, then their long term revenues are secure.

This was backed up by LinkedIn data, which showed enormous growth in Peloton’s employee count year on year:

This was backed up by LinkedIn data, which showed enormous growth in Peloton’s employee count year on year:

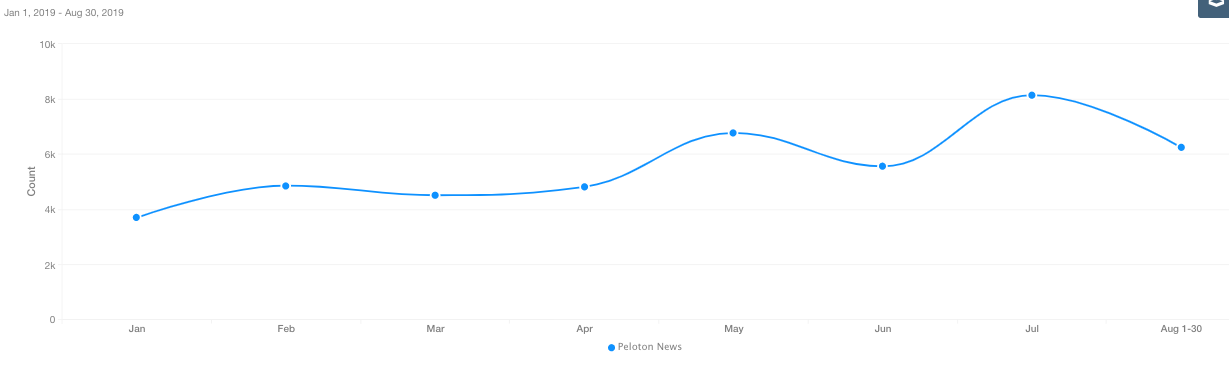

Something else that pointed to really positive momentum was the fact that the amount of press that Meltwater picked up on the company increased steadily since the beginning of 2019.

Something else that pointed to really positive momentum was the fact that the amount of press that Meltwater picked up on the company increased steadily since the beginning of 2019.

Samantha Monk is Meltwater veteran who is currently overseeing the company's Fairhair.ai business line in EMEA. As such she is responsible for finding new ways to monetise Meltwater's data: the largest corpus of news articles and social media posts in the world, enriched with NLP to detect sentiment in 16 different languages, and structured around entities. She is currently working closely with Meltwater's engineering and product teams to explore the application for this unique dataset in finance: for short term trading, for private equity due diligence and ongoing investment monitoring, for credit reporting and for identifying risk and high-growth opportunities around small private companies. Before her current role, Samantha led Meltwater sales and client success teams in Boston, Buenos Aires, Edinburgh and London. In her free time, she maintains a Twitter account (@samantha.monk) focused on providing up to date news around artificial intelligence and machine learning.