Every day there is a major event that will move the markets.

Trade wars, currency wars, oil wars, pandemics, depression levels of unemployment, conspiracy theories; you name it

Are there any more surprises left? Perhaps.

With complete disregard for any of those events, the market keeps marching higher.

Yes, the stock market is a leading indicator of the broader economy, but it seems like the broader consequences of the above events has not yet sunk in.

There is a massive disconnect between the markets and the economy.

For better or worse, the tech giants are at the perfect position to grab even more market share and thrive during the crisis. The high volume of video messaging, Saas, cloud services, content creation and online payments has gifted these giants with record levels of data and recurring revenues. In this new age where data and attention are stronger forms of currency than the fiat money that’s printed out of thin air, the select few are ready with an arsenal of strong balance sheets to pounce on opportunities. As a society that drives forward with innovation, this is inherently not a bad thing but we need to ask the broader consequences of this to the economy and ultimately to the society we live in.

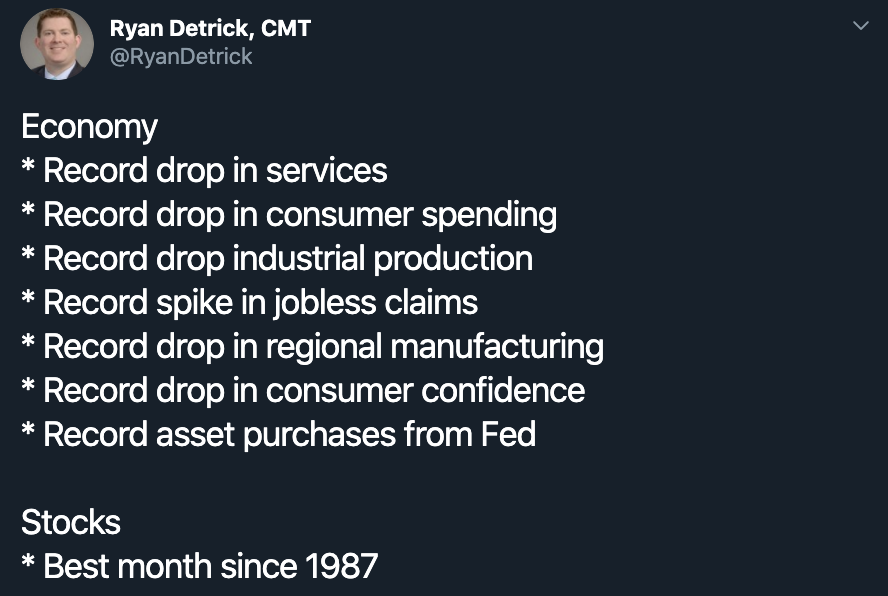

Dozens of millions unemployed, miles-long food lines, businesses shut down, withdrawn guidances and yet the US stock market had the best month since 1987. If a few years ago, someone outlined all the current events and said the index would be rather flat, no one would believe it, and yet here we are.

Food lines Great depression 1929 Vs. Covid crash of 2020.

Bear market rally

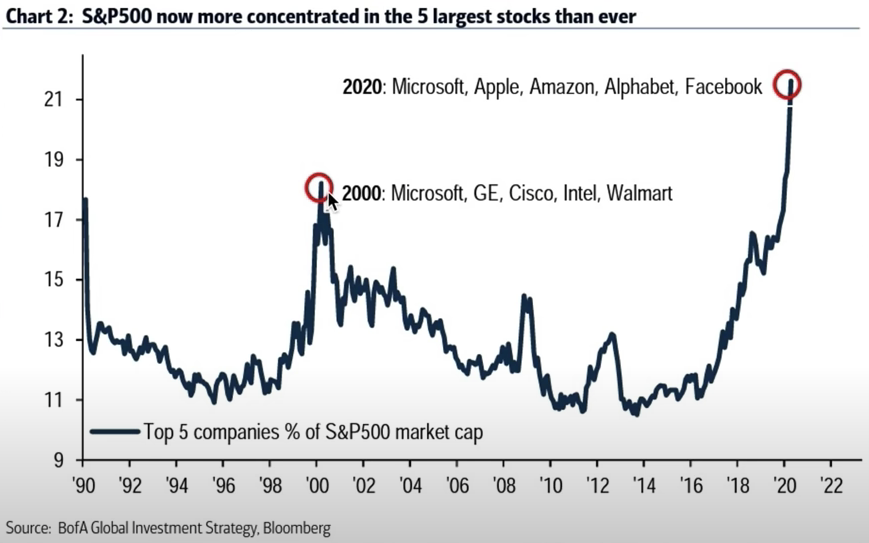

Historically, Bear markets have had significant counter-trend rallies that mystify people, but this recent rally has its unique set of reasons. One of the main reasons being the large concentration of the S&P500 in the 5 largest stocks which draws parallels with the 2000 dot com bubble.

Some reasons to support the recent rally in the mega-cap stocks,

The lockdown would increase their market share and profitability further through a wider and more intensive adaptation of their services.

The possibility the market has discounted their success during the pandemic and given them higher valuations in return while most businesses are struggling.

The majority of the index is concentrated in theses top companies, and therefore, the fresh money coming in from retail investors through ETF’s, bailouts, fed purchases will flow into these companies.

Markets disregarding future knock-on effects even on the tech giants through lower advertising revenue, store shutdown, supply chain problems and lower disposable income.

Systematic changes: work from home, gaming, e-commerce, education, e-conferences.

The fed put. The hope and optimism that central banks will do whatever it takes to maintain liquidity and protect against shocks.

FOMO

Record low levels of interest rates and low bond yields.

Markets have surpassed peak fear and are pricing in more optimistic scenarios through vaccinations, easing lockdown and stimulus.

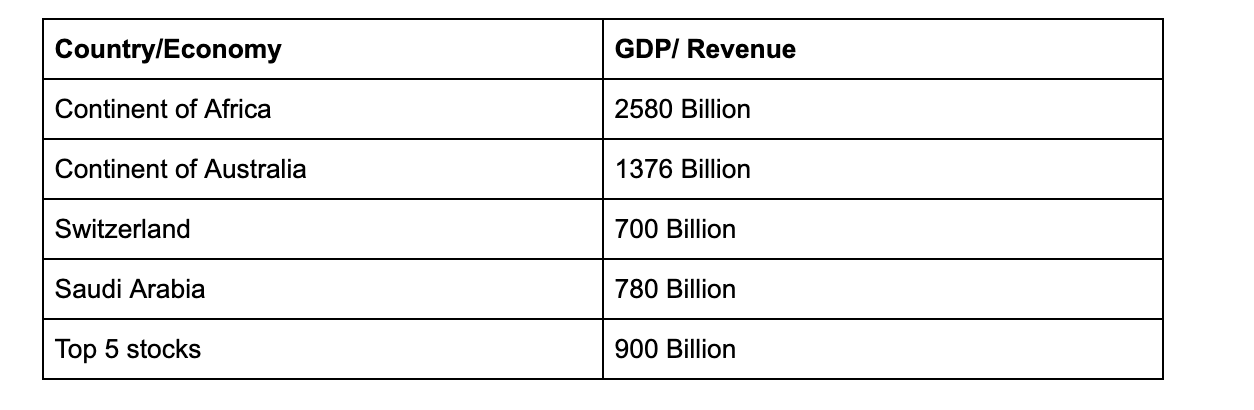

Companies or continents?

Narrowing of market depth as top companies occupy 21% of the whole index.

The top 5 companies represent 21% of the index which contributes primarily to the recent rally. We now have baskets of companies that are much larger than major economies. The dot com bubble had a concentration of 18%. When the concentration increases, the breadth of the market reduces which is a poor signal for future market returns.

The FAAMG stocks are up 10% year to date while the remaining 495 stocks are down 13% year to date

“We don’t have companies, we have continents”- Ash

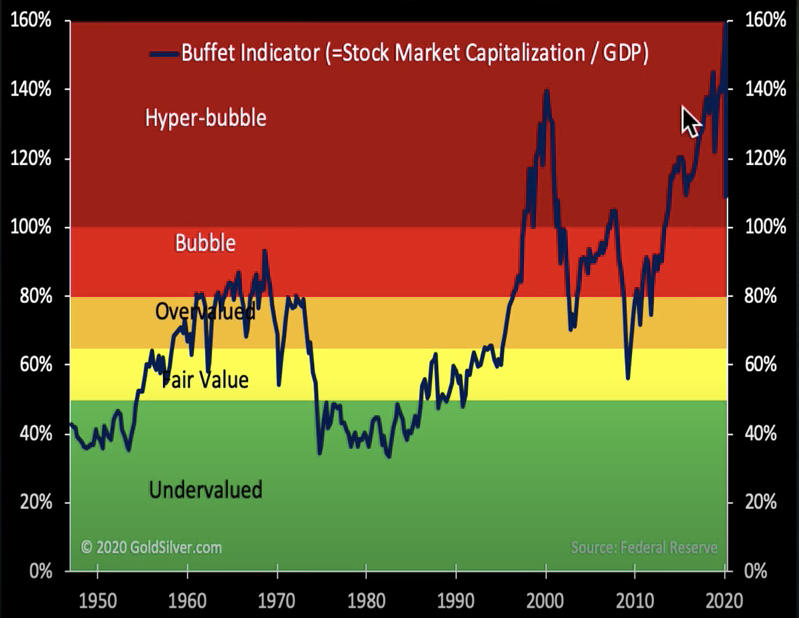

If stocks remain relatively flat amidst contracting GDP’s in nations, the market cap/ GDP ratio would expand further and cause irrational valuations. While the valuations can be justified with higher future earnings, there are doubts whether this is healthy for the overall economy. As seen from the graph, the last time we had valuations as high as this, it did not end well. The buffet indicator indicates the prices are in hyper bubble territory and the legend himself is sitting comfortably on a pile of cash worth $137Billion.

Shiller P/E ratio which shows the average price of a stock to its relative earnings in the S&P 500 is still overvalued. The Shiller P/E ratio repeats throughout history and ranges between a P/E of 24 and 8. After the global financial crisis, the stocks came back within the fair valuation range to be supported again my economic policies particularly favourable to stocks. Either this is the new normal or the valuations will return to their fair values.

I believe many new inventions and ideas that come to life during this time will be praised, years down the line. However, economic growth is ultimately a factor of productivity growth, not excessive money supply and liquidity. Soon enough, markets will likely reflect this through mean reversion.

Can bailout money, “temporary” UBI be classified as real wealth?

How long will the disconnect continue?

Will the stock buybacks that justified higher stock prices continue after the pandemic?

How long can low interest rates last?

Will we see a melt-up or meltdown?

Time will tell.

The great decoupling, 2020

Managing your screen time

On a more personal note, the habits we develop through the excessive use of social media and streaming services will embed into our lives even when the lockdown is lifted without much thought. So, please take some time and reflect on the screen time you spend and question its importance. To keep it simple,

Multiply your social media screentime by the minimum wage in your country.

Use a generous discounting factor if you use social media to promote your business, network or create content.

Multiply that to get stats for a week and a month.

If it’s worth the cost, go ahead. If it’s not, use app limits and restrict phone usage.

aperera Ashain is a Civil engineering graduate from Swinburne university with a passion for fitness and finance. He is currently working as a quality engineer for Bombardier and invests his time in research within the financial sector and the broader economy. Addicted to books, podcasts and learning.