Front, middle, back? Are we in some sort of public transportation?

Since Lehman’s failure more than 10 years have lapsed, during which all compartments of capital markets operations have been reshaped by regulators. But what compartments are we talking about anyway? For non-professionals, capital markets parlance may sound peculiar, and its structure even more. Why is there a distinction between different departments to begin with? Where is such operational complexity coming from, in an industry that has been trying to reduce cost for the better part of the 21st century?

The short answer to those questions is that banks (investment banks especially) have mirrored their internal organization to that of market infrastructures, and are bound to remain compartmentalized in such a way until …well, until something drastic happens in the overall structure of modern markets. Needless to say this is easier said than done, and by the way the major promise of distributed ledger technology is exactly this: a massive simplification of current infrastructures, bringing in its wake a massive reduction in cost.

What are market infrastructures? They are the backbone of modern financial markets, a suite of software applications, patched year after year, or rather decade after decade, to capture the breadth of features necessary to operate public markets.

Let’s take this one step at a time. For an investor to buy a share of stock or a government bond, a few things need to happen:

- there must be a broker to open an account with, and a market to accept and process orders between participants.

- once a transaction is confirmed as executed by an exchange or an intermediary dealer, a middle step called “compensation” takes place. This is basically the step where buyers and sellers positions are calculated based on their respective transactions. Although simple in principle, this step is far from trivial. For example if on the same day I buy 100 shares and sell 50, should the compensation system only register a purchase and a cashflow or two different operations? The answer depends on a number of factors : two clients with distinct legal structures may have a different choices or constraints. Furthermore costs are not identical: settling two dictinct transactions is probably more expensive than settling a single one and a payment. To make a long story short, compensation (also referred to as “clearing”) is a big deal.

- finally assets (and cash) need to be safely transferred from one agent to another, on behalf of their respective customers. Note again that this is not trivial, there must be protection against “double spending”. The 50 shares I bought earlier need to be credited to my account at the same time as they are debited from the seller’s account. And the corresponding cash must follow an identical path in reverse. When a dividend or a coupon is paid, there is an exact number of recipients, which implies a central registry where all shareholders are kept in name, and in real-time.

Every intermediary in the system is regulated, and for good reasons: the end investor, be it an institution or an individual, need to be protected against fraudulent and/or negligent behavior. Which has strong implications for information systems: they need to be 100% reliable, 100% available, and 100% secure.

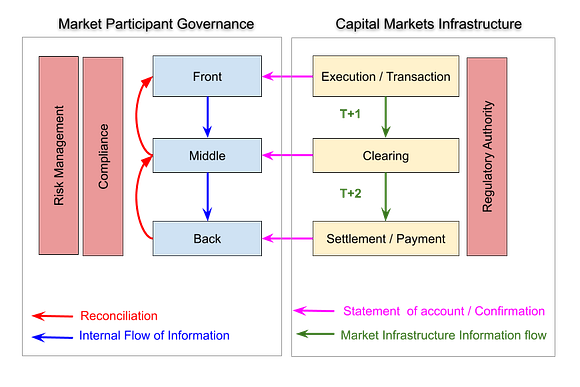

A picture is better than a thousand words, so here is what governance looks like, on both side of the fence (participant / infrastructure):

Capital markets infrastructure is organised around the three basic steps described above. One might wonder why this is the case, the answer is timing. For transactions executed today (T), clearing happens tomorrow (T+1) and settlement the day after (T+2). Again one might ask why is it taking so long? Well, the “settlement cycle” is what it is because it results from 200 years of marginal evolution (some exchanges were already in operations in the early 1800s). When a complex system (IT or otherwise) needs to evolve while being 100% available, it is extremely difficult to organize a Big Bang. Rather stakeholders will plan and deliver one feature at a time, with a tight focus on reliability.

In capital markets all compartments (execution / clearing / settlement) have evolved slowly but surely independently from paper-based to automation, and so from the first days of computerised trading. In case you’re wondering, the communication system in between is an exchange protocol on the SWIFT network (“Fedwire” in the US, “TARGET2” and “T2S” in Europe). Developing a new feature or shortening the settlement cycle requires adapting all three stages and the communication protocol. Quite a feat.

Inside market participants, the distinction front/middle/back reflects the compartmentalization execution/clearing/settlement. However generalized this affirmation is, there are obviously variations here and there. The basic idea holds: every stage of market infrastructure produces a flow of information that is capted by intermediaries and reconciled against the self-produced internal flow. Today, all processes are fully automated (this is known as “straight-through processing”, or STP), but the occasionnal mistake/error wreaks havoc: when something goes wrong with a transaction, there’s little else to do than to check manually, isolate the erroneous data and correct it. Another piece of useful information: most processes in market infrastructure run at night (in their respective time zone). The clearing reconciliation in the middle office of a bank can only start at T+1 when the night batches of the clearing house have produced their results. And so on for settlement. Add to that the fact that T+1 in the US is not T+1 in Europe and vice-versa, and you start getting a picture of how complex (and time-sensitive) things might get. This set of circumstances explains why it is difficult if not impossible for traditional markets to remain open 24/7. Exchanges could very well maintain their electronic trading up and running at night (and some do for certain products), but the clearing/settlement infrastructure is unable to perform its function in real-time. We find here again one of the promises of digital finance: because DLT-based trading has an embedded protection against double-spending, settlement on a block-chain is intrinsically cheaper and faster than on traditional markets. In that context, real-time settlement becomes a real possibility (although DLT does not solve all problems at once, for example the manual processing of errors remains identical).

Regulators have dedicated a lot of time and energy to streamlining market infrastructure layers everywhere, because those are literally the basic building blocks of modern markets. Making the different systems interoperable, reducing the settlement cycle to decrease credit risk, standardizing protocols have become regulatory levers for increased efficiency with three stated objectives : reducing transaction costs, increasing transparency and reducing risk. Are we in some sort of public transportation service? Well, one could be tempted to acquiesce at this statement, considering the necessary implication of public policies (and political will) to make all this happen.